Cryptocurrency Should It Have a Place in Your Personal Finance Plan?

Let’s be honest — cryptocurrency has had more plot twists than a prime-time drama. From Bitcoin’s meteoric rise to the spectacular collapse of FTX, from regulatory crackdowns to institutional embrace, crypto has kept investors on a perpetual emotional rollercoaster. But here in mid-2026, something genuinely different is happening. The rules of the game are finally being written — and that changes everything. Or does it?

At Your Career Place, we believe that smart financial decisions start with clear, unbiased information. So today, we’re diving deep into the world of cryptocurrency — what’s changed, what hasn’t, and whether it deserves a spot in your personal finance strategy. We’ll hear from both the optimists (the “Crypto Boomers”) and the skeptics (the “Crypto Doomers”) so you can decide for yourself.

What’s Actually New in Crypto Right Now?

The biggest story in crypto in 2026 isn’t a price surge or a crash — it’s regulation. For years, the crypto world operated in a legal gray zone, with regulators playing whack-a-mole with exchanges and token issuers. That era is ending fast.

Here are the key developments shaping the landscape right now:

- The GENIUS Act is now law. Signed in July 2025, the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act created the first federal framework for U.S. dollar-backed stablecoins. Issuers must be licensed, maintain 1:1 reserves in cash or short-term U.S. Treasuries, and undergo regular audits. If a stablecoin issuer goes bankrupt, token holders now have legal protections — a first in U.S. crypto history.

- The SEC and CFTC drew the map. In March 2026, the two agencies issued a landmark joint interpretation officially classifying Bitcoin and Ethereum as “digital commodities” — not securities. This is huge. It means they fall under the CFTC’s jurisdiction, not the SEC’s, and clears the path for broader institutional participation.

- Europe went first with MiCA. The EU’s Markets in Crypto-Assets regulation became fully effective on July 1, 2026 — the world’s first comprehensive crypto rulebook. It covers everything from stablecoin reserves to exchange licensing requirements.

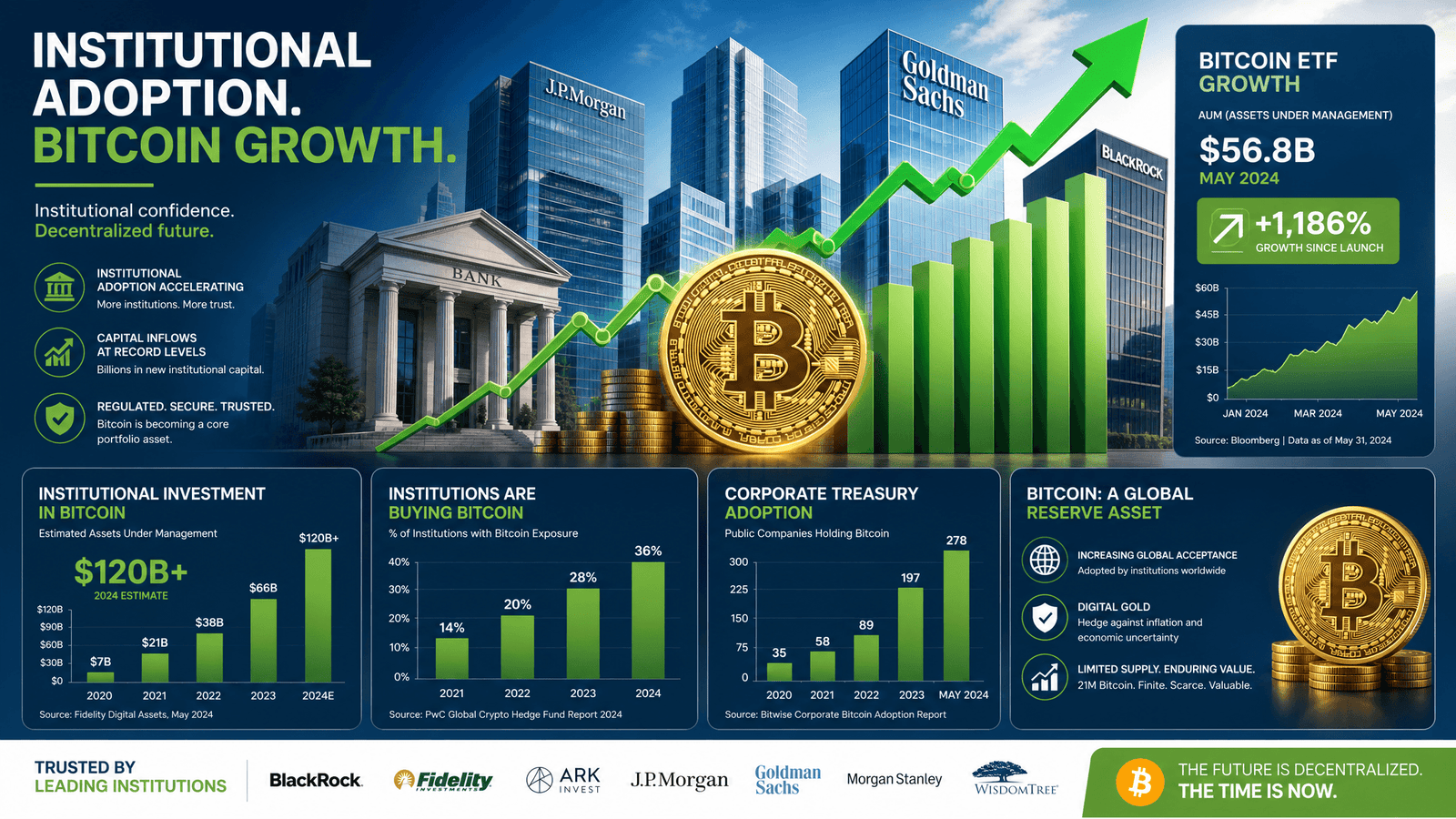

- Spot Bitcoin and Ethereum ETFs are mainstream. These regulated investment vehicles have become the primary on-ramp for institutional money. Total assets in crypto exchange-traded products could exceed $400 billion globally by year-end, with wealth management platforms projected to drive over $50 billion in new inflows.

- Financial advisors are warming up. According to the 2026 Bitwise/VettaFi survey, 32% of financial advisors now allocate to crypto in client accounts — up from 22% in 2024. And 99% of those already invested plan to maintain or increase their exposure.

- Tokenized real-world assets are booming. Solana’s market for tokenized real-world assets (RWAs) — think stocks, bonds, and real estate on a blockchain — grew fourfold to $3.62 billion in just the first half of 2026, with enterprise users like Visa and SoFi on board.

So the landscape has genuinely shifted. But does that mean you should rush out and buy Bitcoin? Not so fast. Let’s hear both sides.

The Boomer Perspective: “This Is the Dawn of a New Financial Era”

The optimists — let’s call them Crypto Boomers — see 2026 as a turning point. Their argument: crypto has finally grown up, and the institutional era is just beginning.

Here’s the Boomer case in plain English:

Regulation is a feature, not a bug. Yes, new rules mean more compliance costs. But they also mean legitimacy. When the SEC and CFTC officially classify Bitcoin as a commodity, it signals to pension funds, endowments, and wealth managers that it’s safe to participate. That’s a massive pool of capital that was previously sitting on the sidelines.

Institutions aren’t just dipping their toes in — they’re diving. BlackRock, JPMorgan, and Fidelity aren’t known for chasing fads. They’re building infrastructure on Ethereum, launching crypto ETFs, and integrating digital assets into standard model portfolios. When the world’s largest asset managers are all-in, it’s hard to dismiss crypto as a fringe phenomenon.

Bitcoin as “digital gold” is becoming a mainstream idea. Analysts at Standard Chartered maintain a Bitcoin price target of around $150,000. The argument: just as gold serves as a store of value and hedge against currency debasement, Bitcoin — with its fixed supply of 21 million coins — can serve the same role in a digital age. With global debt levels at historic highs and central banks continuing to print money, the appeal of a scarce, decentralized asset is real.

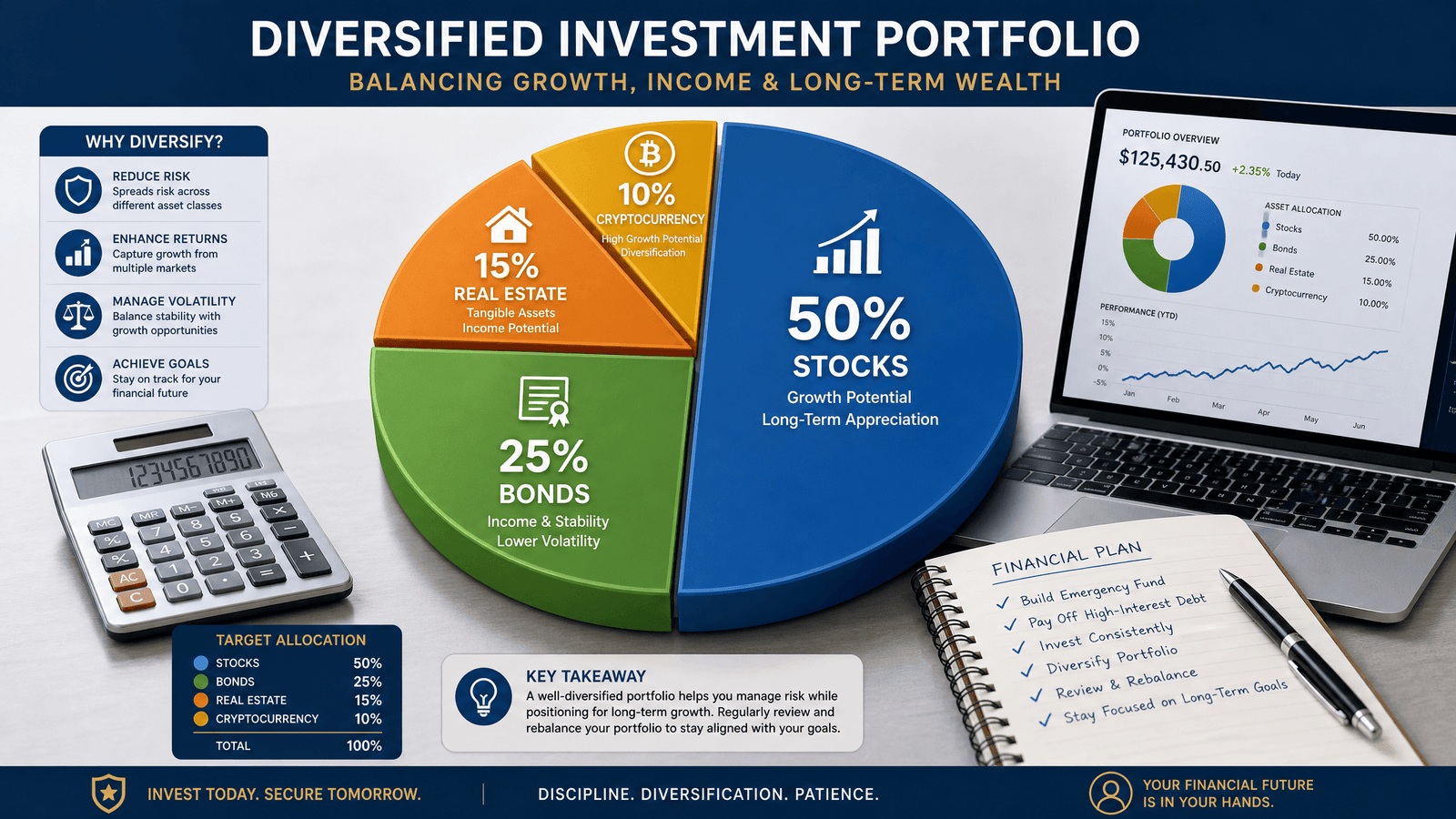

Small allocations can improve your portfolio. Research from Fidelity Digital Assets suggests that a 1–3% allocation to Bitcoin has historically improved risk-adjusted returns in a diversified portfolio. The key word is “small.” You’re not betting the farm — you’re adding a high-potential, high-risk ingredient to an otherwise balanced recipe.

Stablecoins are becoming the internet’s dollar. Regulated stablecoins — fully backed, audited, and legally protected — are quietly becoming the plumbing of global commerce. Their market cap is projected to reach $1–2 trillion by 2027. For everyday people, this means faster, cheaper international money transfers and new ways to earn on idle cash.

The Boomer bottom line: Crypto has crossed the threshold from speculation to legitimate asset class. Missing out entirely could mean leaving real long-term gains on the table.

The Doomer Perspective: “Don’t Let the Suit and Tie Fool You”

The skeptics — the Crypto Doomers — aren’t necessarily anti-technology. They just think the risks are being systematically underplayed, and that a regulatory stamp of approval doesn’t make a volatile asset safe.

Here’s the Doomer case:

Volatility hasn’t gone anywhere. In June 2026, U.S. spot Bitcoin ETFs experienced a brutal 10-day outflow streak totaling $2.73 billion. Research now shows that ETF flows can influence up to 45% of weekly Bitcoin price movements. In other words, when big institutions decide to sell, they can crater the market — and retail investors get caught in the crossfire.

The price forecasts are all over the map. Standard Chartered says Bitcoin could hit $150,000. Other veteran analysts warn it could crash back to $23,000–$25,000 in a broader market downturn. When credible experts’ predictions differ by a factor of six or more, that’s not an investment — that’s a coin flip with extra steps.

Crypto still moves with the stock market. The promise that Bitcoin would be an “uncorrelated” asset — one that zigs when stocks zag — hasn’t materialized. Bitcoin and major altcoins continue to trade as high-beta risk assets, meaning they fall harder than stocks during downturns. If you’re buying crypto as a hedge against a market crash, you may be in for a rude awakening.

Regulation creates new problems, not just solutions. The GENIUS Act’s requirement that stablecoins hold reserves in U.S. Treasuries conflicts with the EU’s MiCA framework, which requires some reserves in EU banks. This forces issuers into costly, fragmented operations. And the GENIUS Act’s prohibition on paying yield on stablecoins has eliminated a popular source of passive income for retail users — one of the main reasons everyday people were using them in the first place.

Tax complexity is a real headache. Global regulators — through frameworks like the OECD’s CARF and the EU’s DAC8 — are getting serious about crypto tax compliance. Every transaction may be a taxable event. If you’re not keeping meticulous records, you could face a nasty surprise at tax time.

The Doomer bottom line: A regulatory framework doesn’t make a speculative asset safe. The casino has a dress code now, but it’s still a casino.

So What Should You Actually Do? Key Takeaways for Your Personal Finance Plan

At Your Career Place, we’re not here to tell you what to do with your money — that’s between you and a qualified financial advisor. But we can give you a framework for thinking through the decision clearly.

1. Know your “why” before you buy. Are you looking for a speculative bet with high upside potential? A long-term store of value? Or are you just feeling FOMO because your coworker won’t stop talking about Bitcoin? Your motivation matters. Speculative money and retirement savings should never be in the same bucket.

2. If you invest, keep it small. Most financial advisors who recommend crypto suggest limiting it to 1–5% of your total portfolio. This is enough to benefit if crypto takes off, but not enough to derail your financial future if it crashes. Think of it as a high-risk, high-reward satellite position around a core of diversified, traditional investments.

3. Dollar-cost averaging is your friend. Instead of trying to time the market (spoiler: nobody can), invest a fixed amount on a regular schedule — say, $50 or $100 per month. This strategy, called dollar-cost averaging (DCA), smooths out your entry price and removes the emotional temptation to buy high and sell low.

4. Choose regulated vehicles. In 2026, you have better options than ever. Spot Bitcoin and Ethereum ETFs held in a traditional brokerage account are the simplest and most secure way to get exposure. You don’t have to worry about losing your private keys or getting hacked. If you prefer direct ownership, stick to reputable, regulated exchanges.

5. Understand the tax implications. Every time you sell, trade, or even spend cryptocurrency, it may trigger a taxable event. Use crypto tax software or work with a tax professional who understands digital assets. Ignorance is not a defense with the IRS.

6. Never invest money you can’t afford to lose. This isn’t a cliché — it’s the most important rule in crypto. The difference between a $23,000 Bitcoin and a $150,000 Bitcoin is real. So is the difference between a $100,000 Bitcoin and a $30,000 one. If a 70% drop would devastate your finances or your sleep, you’re overexposed.

7. Stay educated. The crypto landscape changes faster than almost any other financial sector. Regulatory updates, new products, and market dynamics can quickly shift your risk profile. Make it a habit to check in on your crypto holdings and the broader landscape at least quarterly.

The Bottom Line

Cryptocurrency in 2026 is not the Wild West it once was. It’s a regulated, institutionally recognized asset class with real use cases, real risks, and real opportunities. The Boomers are right that something fundamental has changed. The Doomers are right that volatility and uncertainty remain very real.

The truth, as usual, lives somewhere in the middle. For most working professionals, a small, disciplined allocation to crypto — through regulated vehicles, with money you can afford to lose — is a reasonable way to participate in what could be a transformative technology. For others, the volatility and complexity simply aren’t worth it, and that’s a perfectly valid choice too.

Whatever you decide, make sure it’s an informed decision — not one driven by hype, fear, or your neighbor’s hot tip. That’s what financial literacy is all about, and it’s exactly what we’re here for at Your Career Place.

Have questions about building a balanced personal finance strategy? Explore more resources at Your Career Place — your partner in career and financial growth.