Budgeting in 2026

How to Take Control of Your Money When Everything Costs More

By Your Career Place | Personal Finance Series

Let’s be honest — budgeting has never been the most exciting topic at the dinner table. But in 2026, it might just be the most important one. With household debt hitting a staggering $18.8 trillion, 51% of Americans living paycheck to paycheck, and food prices still running more than 18% above 2022 levels, the question isn’t whether you need a budget — it’s whether your current budget is actually working for you.

At Your Career Place, we believe that financial wellness and career success go hand in hand. Whether you’re just starting out, navigating a career transition, or planning for the years ahead, understanding how to manage your money in today’s economic climate is a skill that pays dividends every single day. This week, we’re diving deep into the world of budgeting — what’s changed, what’s working, and what the experts are saying right now.

The State of American Household Finances: A Reality Check

Before we talk strategy, let’s look at where things actually stand. The numbers paint a sobering picture:

- Total U.S. household debt reached $18.8 trillion at the end of 2025 — up $191 billion in a single quarter.

- The average household credit card debt is now $11,507, with 7.13% of balances falling into serious delinquency.

- The personal savings rate has dropped to just 4.5% of disposable income — a 23% decline in just one year.

- A full 29% of Americans carry more credit card debt than emergency savings.

- Only 45% of people feel confident they could cover an unexpected $1,000 expense.

And yet — here’s the silver lining — 53% of Americans now have a formal budget in 2026, up from 46% just a year ago. People are waking up to the reality that wishing for financial stability isn’t enough. You have to plan for it.

The economic pressures driving this shift are real. Housing costs require an annual income of $121,400 just to afford a typical home. Energy bills jumped 12% in 2025. Vehicle insurance costs rose 12.3% year-over-year. Healthcare premiums could more than double for some households if tax credit subsidies expire. This is what economists are calling an “affordability crisis” — and it’s hitting working-class families the hardest.

The “K-Shaped” Economy: Are You on the Right Side?

One of the most important concepts to understand right now is what economists call the “K-shaped” economy. Picture the letter K: the top arm goes up, the bottom arm goes down. That’s exactly what’s happening to American consumers.

Higher-income households — those with significant assets, strong job security, and investment portfolios — have largely weathered the storm. They’re still spending on travel, experiences, and discretionary items. The top 20% of households now hold 72% of total household wealth, the highest concentration since 1989.

Meanwhile, lower-income and middle-class households have burned through their pandemic-era savings and are increasingly relying on credit cards and “Buy Now, Pay Later” services just to cover routine expenses. If you feel like you’re working harder but falling further behind, you’re not imagining it — and you’re not alone.

This is exactly why the team at Your Career Place emphasizes both career development and financial literacy. Increasing your earning potential is just as important as controlling your expenses — and we’ll come back to that point.

The Boomer Perspective: “Budgeting Has Always Been the Answer”

If you grew up in a household where your parents tracked every dollar in a paper ledger, you might recognize the Boomer perspective on budgeting: discipline, consistency, and living within your means are timeless principles that never go out of style — and the data backs them up.

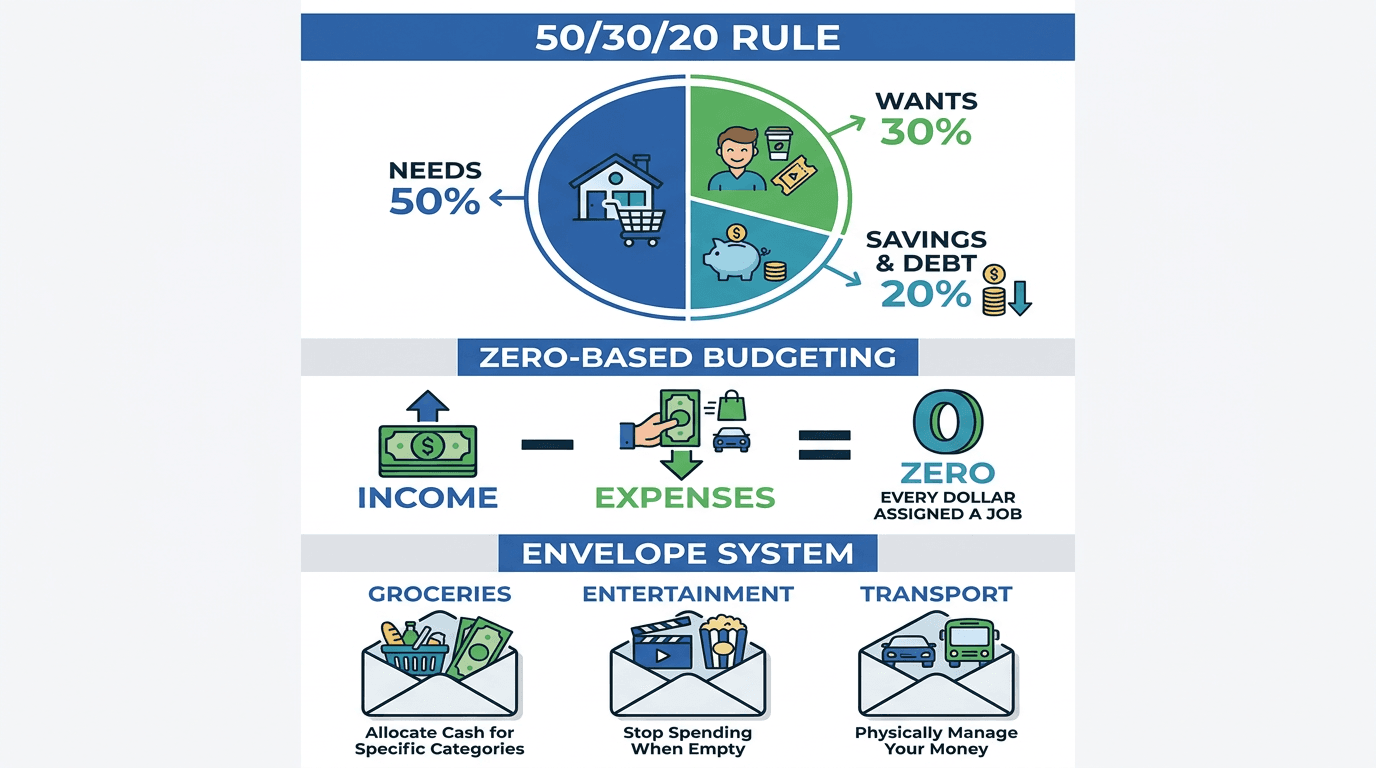

The good news from the Boomer camp is that the fundamentals of budgeting are simpler than ever to implement. The classic 50/30/20 rule — allocating 50% of your take-home pay to needs, 30% to wants, and 20% to savings and debt repayment — remains one of the most effective frameworks available. It’s not flashy, but it works.

And the tools available today? They’re extraordinary compared to what previous generations had. Spreadsheets (still used by 35% of budgeters) are free, flexible, and powerful. Apps like YNAB (You Need A Budget), Monarch Money, and Empower can automate tracking, categorize spending automatically, and even use AI to identify where your money is leaking.

The Boomer optimist would also point to this: 53% of Americans now have a budget. That’s a meaningful cultural shift. More people are taking ownership of their finances, and that’s always a positive sign. The tools exist, the knowledge is accessible, and the motivation — driven by economic necessity — has never been stronger.

Financial experts echo this optimism. Automating your savings so that money moves to a savings or investment account before you can spend it — the classic “pay yourself first” strategy — is more achievable than ever. Setting up automatic 401(k) contributions to capture your full employer match is essentially free money. These are wins that are available to almost everyone, regardless of income level.

The Boomer takeaway: Stop waiting for the perfect moment to start budgeting. The best budget is the one you actually use.

The Doomer Perspective: “Budgeting Can’t Fix a Broken System”

Now let’s hear from the other side — because ignoring the structural challenges doesn’t make them go away.

The Doomer perspective on budgeting in 2026 starts with a hard truth: you can’t budget your way out of a housing crisis. When 37.1 million households are considered “cost-burdened” — spending more than 30% of their income on housing — no amount of cutting back on lattes is going to close that gap. The math simply doesn’t work.

Consider this: the average U.S. household spent $78,535 in 2024, with housing alone consuming 33.4% of that ($26,266 annually). Add transportation at 17% and food at nearly 13%, and you’ve already allocated nearly two-thirds of the average household budget to three non-negotiable categories — before a single discretionary dollar is spent.

The Doomer would also point to the psychological toll. 80% of Americans reported financial anxiety in 2025, and 52% worried about money every single day. Chronic financial stress has real consequences for health, relationships, and job performance. Telling someone who is already stretched thin to “just make a budget” can feel dismissive of the very real structural barriers they face.

There’s also the debt spiral problem. With credit card interest rates still elevated and 7.13% of balances in serious delinquency, many households are in a situation where minimum payments barely cover interest charges. Budgeting helps you stop digging the hole deeper — but it doesn’t automatically fill in the hole that’s already there.

And let’s talk about income inequality. The K-shaped economy isn’t just a talking point — it’s a measurable reality. When the top 20% hold 72% of all household wealth, the budgeting advice that works for a $150,000-a-year household may be completely irrelevant to someone earning $45,000. Generic budgeting advice often fails to account for this reality.

The Doomer takeaway: Budgeting is necessary but not sufficient. Systemic change — in housing policy, healthcare costs, and wage growth — is equally important for long-term financial health.

What Actually Works: Practical Budgeting Strategies for 2026

Whether you lean Boomer or Doomer, the practical reality is that a well-designed budget is one of the most powerful tools available to you right now. Here’s what financial experts are recommending for 2026:

1. Choose a Method and Stick With It

The best budgeting system is the one you’ll actually use. Options include:

- 50/30/20 Rule: Simple, balanced, and great for beginners.

- Zero-Based Budgeting: Every dollar gets a job. Favored by YNAB users for its intentionality.

- Envelope System: Physical or digital envelopes for each spending category. Great for visual learners.

- Spreadsheet Tracking: Maximum flexibility, zero cost. Still the most popular method overall.

2. Leverage Technology — Including AI

Budgeting apps have evolved dramatically. Monarch Money and Origin offer comprehensive financial hubs with AI assistance, investment tracking, and collaborative features for couples. Rocket Money excels at identifying and canceling unwanted subscriptions. Even Google’s Gemini can help you build custom budget trackers and analyze your spending patterns.

3. Automate Everything You Can

Set up automatic transfers to savings on payday. Automate bill payments to avoid late fees. Contribute automatically to your 401(k) — at minimum, enough to capture your full employer match. Automation removes willpower from the equation.

4. Attack High-Interest Debt Aggressively

With average credit card debt at $11,507 per household, prioritizing payoff of high-interest balances is one of the highest-return financial moves available. Consider the avalanche method (highest interest rate first) or the snowball method (smallest balance first for psychological wins).

5. Review and Adjust Monthly

A budget is a living document, not a one-time exercise. Review it monthly, adjust quarterly, and treat every unexpected expense as data — not a failure. Life changes, and your budget should too.

6. Don’t Forget the Income Side

At Your Career Place, we always remind our community: budgeting is about both sides of the equation. Cutting expenses has a floor — you can only cut so much. But growing your income has no ceiling. Whether it’s negotiating a raise, developing new skills, or exploring side income opportunities, investing in your earning potential is one of the most powerful budgeting moves you can make.

Key Takeaways

Here’s what we want you to walk away with from this week’s Your Career Place personal finance deep-dive:

- The economic environment is genuinely challenging — rising debt, persistent inflation in housing and food, and a K-shaped economy mean that financial stress is real and widespread. You’re not failing; the system is hard.

- Budgeting adoption is rising — 53% of Americans now have a formal budget, up from 46% last year. This is a positive trend, and joining that group puts you ahead of the curve.

- The right tools make a difference — from free spreadsheets to AI-powered apps like Monarch Money and YNAB, there’s a budgeting solution for every style and income level.

- Automation is your best friend — automate savings, bill payments, and retirement contributions to remove friction and build wealth on autopilot.

- Tackle debt strategically — with credit card delinquencies rising, getting ahead of high-interest debt is one of the most impactful financial moves you can make right now.

- Income growth matters as much as expense control — don’t just budget harder; invest in your career and earning potential too.

Financial wellness isn’t a destination — it’s a practice. And like any practice, it gets easier and more effective the more consistently you show up for it. The team at Your Career Place is here to support you on both the career and financial sides of that journey.

What budgeting method works best for you? Share your experience in the comments below — we’d love to hear from the Your Career Place community!

Sources: YouGov Consumer Spending Trends 2026 | Federal Reserve Bank of New York Household Debt Report Q4 2025 | WalletHub Budgeting Statistics | Forbes Advisor Best Budgeting Apps 2026 | CBS News Affordability Crisis 2025 | Minneapolis Fed K-Shaped Economy Analysis | California DFPI 6-Step Financial Plan 2026 | Visual Capitalist State of U.S. Household Finances 2025