Real Estate: Is Now the Right Time to Buy, Sell, or Invest?

By Your Career Place | May 27, 2026

If you’ve been watching the housing market lately, you’ve probably noticed something strange: it feels like the market is holding its breath. After years of frenzied bidding wars, rock-bottom mortgage rates, and skyrocketing home prices, 2026 has ushered in what many economists are calling the “Great Housing Reset.” Things are slowing down — but that doesn’t mean they’re getting easier.

Whether you’re a first-time buyer trying to break into the market, a homeowner wondering if now is the time to sell, or an investor looking for your next opportunity, the real estate landscape right now is full of both promise and pitfalls. At Your Career Place, we believe that understanding your financial environment is just as important as understanding your career — because the two are deeply connected. So let’s break down what’s really happening in real estate right now, and what it means for your wallet.

What’s Actually Happening in the Housing Market Right Now

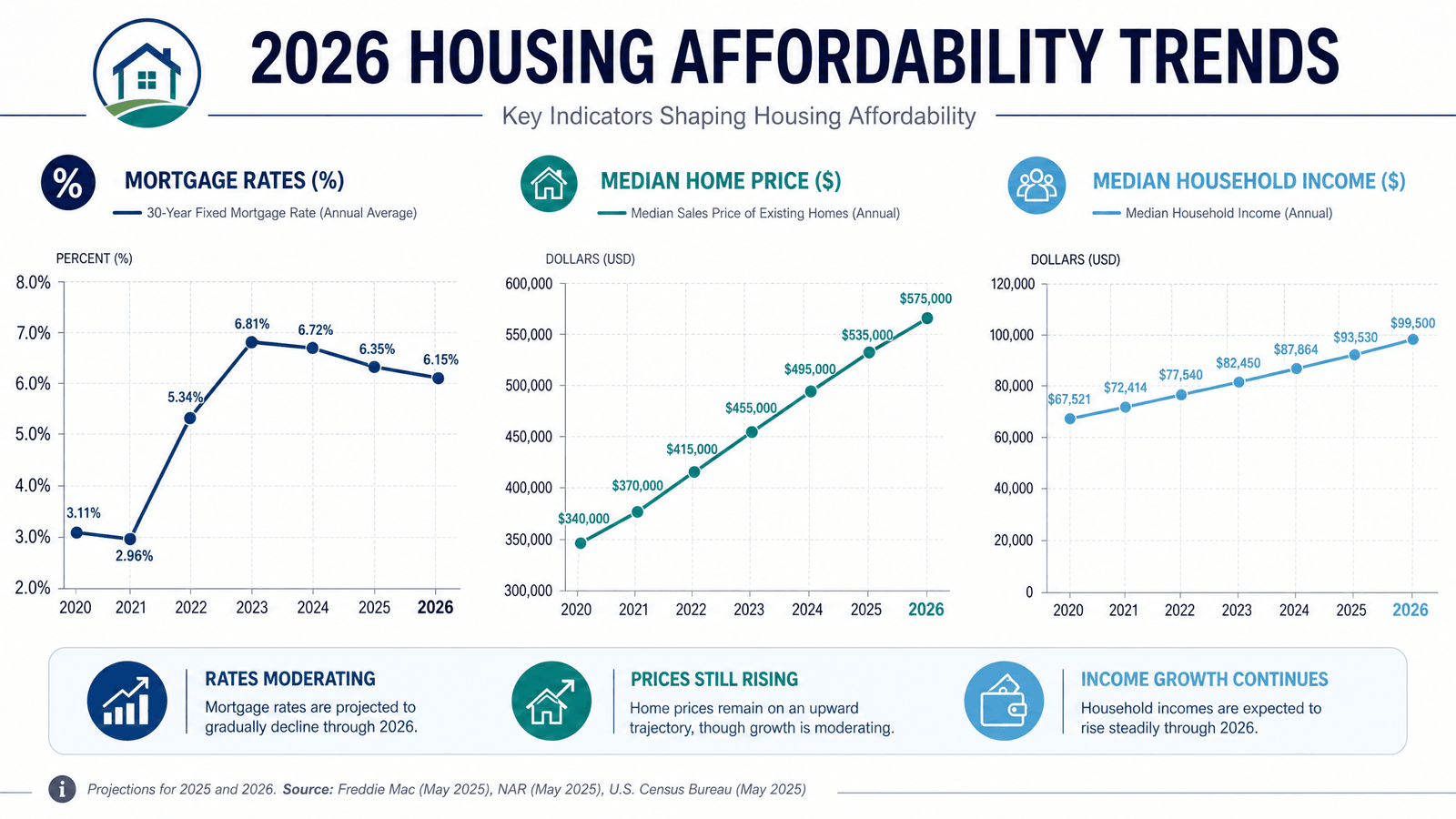

The headline numbers tell a complicated story. Mortgage rates on a 30-year fixed loan are hovering around 6.5% as of late May 2026 — down from recent peaks, but still more than double the sub-3% rates many buyers locked in during the pandemic era. Home prices nationally are still rising, but slowly: forecasts range from a modest 1% to 4% appreciation for the year, depending on who you ask.

Inventory is finally starting to loosen up. More homes are coming onto the market as the “mortgage rate lock-in effect” — where homeowners refused to sell because they didn’t want to give up their low-rate loans — begins to fade. Life events like job changes, divorces, and growing families are forcing moves regardless of rates. That’s good news for buyers who’ve been frustrated by a lack of options.

But here’s the catch: even with more homes available, affordability remains at a historic crisis point. The ratio of median home prices to household incomes is nearly 6.0 — far above the historical norm of around 3.0 to 4.0. According to the National Association of REALTORS® (NAR), first-time homebuyers now make up just 21% of the market, a record low. The dream of homeownership is becoming harder to reach for millions of Americans.

Meanwhile, a structural housing shortage of approximately 1.2 million units continues to put a floor under prices. Even if demand softens, there simply aren’t enough homes to go around — which means a dramatic price crash is unlikely in most markets.

The Regional Picture: It’s Not One Market, It’s Many

One of the most important things to understand about real estate in 2026 is that national averages can be deeply misleading. The market in Cleveland, Ohio looks nothing like the market in Austin, Texas.

Sun Belt markets — particularly in Texas and Florida — that boomed during the pandemic are now cooling. A surge in new construction, combined with soaring homeowners’ insurance costs (driven by climate-related risks), has softened prices in some of these areas. In contrast, Midwest and Great Lakes cities like Cleveland and St. Louis are showing remarkable resilience, offering more affordable entry points and stronger relative demand.

For investors, the Emerging Trends in Real Estate® 2026 report from PwC and the Urban Land Institute identifies Dallas/Fort Worth, Jersey City, Miami, Brooklyn, and Houston as top markets for investment and development prospects. The focus has shifted from chasing appreciation to finding cash flow — a back-to-basics approach that seasoned investors know well.

The Boomer Perspective: Reasons to Be Optimistic

If you’re someone who’s been around long enough to remember 18% mortgage rates in the early 1980s, today’s 6.5% might not seem so scary. And there are genuinely good reasons to feel optimistic about real estate right now.

Prices aren’t crashing — and probably won’t. That 1.2 million unit housing deficit isn’t going away overnight. As long as there’s a fundamental shortage of homes, prices have a built-in support system. Even the most pessimistic forecasters (like J.P. Morgan) are predicting flat prices, not a collapse.

Wage growth is finally catching up. For the first time in years, wage growth in 2026 is expected to outpace home price appreciation. That means affordability, while still strained, is slowly improving. If you can afford to wait a bit longer, the math may get a little better.

Mortgage rates are trending down. The Federal Reserve has already cut rates, and while it’s being cautious about further cuts, the direction of travel is downward. Institutions like Fannie Mae are forecasting rates settling around 6.0% by year-end, with S&P Global projecting as low as 5.77%. If you buy now and rates drop further, you can always refinance.

Policy is moving in the right direction. The bipartisan 21st Century ROAD to Housing Act recently passed the Senate, aiming to increase housing supply by streamlining zoning and reducing regulatory barriers. The White House has also issued executive orders to remove obstacles to affordable home construction. These aren’t quick fixes, but they signal that Washington is finally taking the supply problem seriously.

At Your Career Place, we often talk about the importance of long-term thinking in your career — and the same applies to real estate. Historically, real estate has been one of the most reliable wealth-building tools available to everyday Americans. If you’re financially ready and planning to stay put for at least five to seven years, buying in today’s market can still make a lot of sense.

The Doomer Perspective: Reasons to Proceed with Caution

Of course, optimism needs to be tempered with realism. There are serious headwinds in the housing market that deserve honest attention.

Affordability is at a breaking point. A median-priced home now requires an income that exceeds what the typical first-time buyer earns by more than $20,000. Nearly 30% of buyers now rely on gift funds from family members for their down payment, and 37% are planning to purchase homes with someone other than a spouse — pooling resources just to get a foot in the door. This isn’t a healthy market; it’s a market where the rules of the game have fundamentally changed.

The rental market offers little relief. If you can’t afford to buy, renting isn’t much better. According to research from Harvard’s Joint Center for Housing Studies, a record 22.7 million renter households — nearly half of all renters — are “cost-burdened,” spending more than 30% of their income on rent. Of those, 12.1 million are “severely burdened,” spending over half their income on housing. That leaves almost nothing for savings, emergencies, or retirement.

Geopolitical and economic uncertainty is keeping rates elevated. The Federal Reserve’s cautious stance isn’t just about domestic inflation — geopolitical tensions are pushing up Treasury yields, which in turn keeps mortgage rates stubbornly high. The era of cheap money appears to be over, and the “new normal” for mortgage rates may be in the 5.5% to 6.5% range for the foreseeable future.

Insurance costs are becoming a hidden crisis. In many parts of the country — particularly coastal areas and regions prone to wildfires and flooding — homeowners’ insurance costs have skyrocketed or become unavailable altogether. This is a risk that many buyers aren’t fully accounting for when they calculate the true cost of homeownership.

Institutional investors aren’t going away. While new legislation restricts large institutional investors (those owning 350+ single-family homes) from acquiring new properties, analysts note this affects less than 2% of the national housing stock. The structural forces that made single-family homes attractive to Wall Street haven’t disappeared.

The team at Your Career Place always encourages people to make financial decisions based on their own situation — not on pressure, fear of missing out, or what their neighbors are doing. If buying a home would stretch your budget to the breaking point, it’s okay to wait. Renting while you build savings and improve your financial position is a legitimate strategy.

Creative Strategies Buyers Are Using in 2026

Faced with these challenges, today’s homebuyers are getting creative — and there’s no shame in that. Here are some of the approaches people are using to navigate this tough market:

- Co-buying: Purchasing a home with a friend, sibling, or other non-spouse partner to split costs and qualify for a larger loan.

- Gift funds: Accepting down payment assistance from family members — a strategy used by nearly 30% of buyers.

- AI-powered tools: Over a quarter of buyers are now using AI tools to compare mortgage rates, analyze neighborhoods, and identify undervalued properties.

- Targeting affordable markets: Looking beyond the obvious hot spots to find value in Midwest and Great Lakes cities where prices are more reasonable.

- Adjustable-rate mortgages (ARMs): Accepting a lower initial rate with the expectation of refinancing when fixed rates drop further.

Key Takeaways: What Should You Do?

The 2026 housing market doesn’t offer easy answers — but it does offer clarity if you know what to look for. Here’s what the Your Career Place team thinks you should keep in mind:

- Know your local market. National headlines are almost irrelevant to your specific situation. Research what’s happening in the specific city and neighborhood you’re interested in. Prices, inventory, and trends vary enormously by location.

- Run the real numbers. Don’t just look at the mortgage payment. Factor in property taxes, insurance (which is rising fast in many areas), HOA fees, maintenance, and the opportunity cost of your down payment. Make sure homeownership actually makes financial sense for you.

- Don’t try to time the market. Waiting for rates to drop to 4% or 5% could mean waiting years — and prices may rise in the meantime. If you’re financially ready and planning to stay for the long term, the best time to buy is when it makes sense for your life.

- If you’re renting, invest the difference. If buying doesn’t make sense right now, make sure you’re putting the money you’re saving (compared to owning) to work in the stock market or other investments. Don’t let renting become an excuse to avoid building wealth.

- For investors, focus on cash flow. The days of buying anything and watching it appreciate are over in most markets. Look for properties that generate positive cash flow from day one, in markets with strong job growth and population trends.

- Stay informed. The housing market is changing rapidly. Policy changes, interest rate decisions, and economic shifts can all affect your options. Keep learning — and that’s exactly what Your Career Place is here to help you do.

Real estate has always been one of the most powerful tools for building long-term wealth — but it’s never been a guaranteed path, and it’s never been without risk. In 2026, the stakes feel higher than ever, and the decisions feel harder. But with the right information and a clear-eyed view of your own financial situation, you can navigate this market with confidence.

At Your Career Place, we’re committed to giving you the honest, practical financial insights you need to make smart decisions — whether that’s about your career, your investments, or the roof over your head. Stay tuned for more weekly personal finance updates, and don’t hesitate to share this post with someone who’s trying to figure out their next move in today’s housing market.

Have questions or thoughts about the real estate market? Drop a comment below — we’d love to hear from you.