Inflation in 2026

Is Your Wallet Winning or Losing the Battle?

By Your Career Place | June 2026

You’ve felt it at the grocery store. You’ve felt it at the gas pump. You’ve definitely felt it when your rent renewal letter arrived. Inflation — that slow, relentless erosion of your purchasing power — is still very much a part of everyday life in 2026, and it’s shaping financial decisions for millions of working Americans.

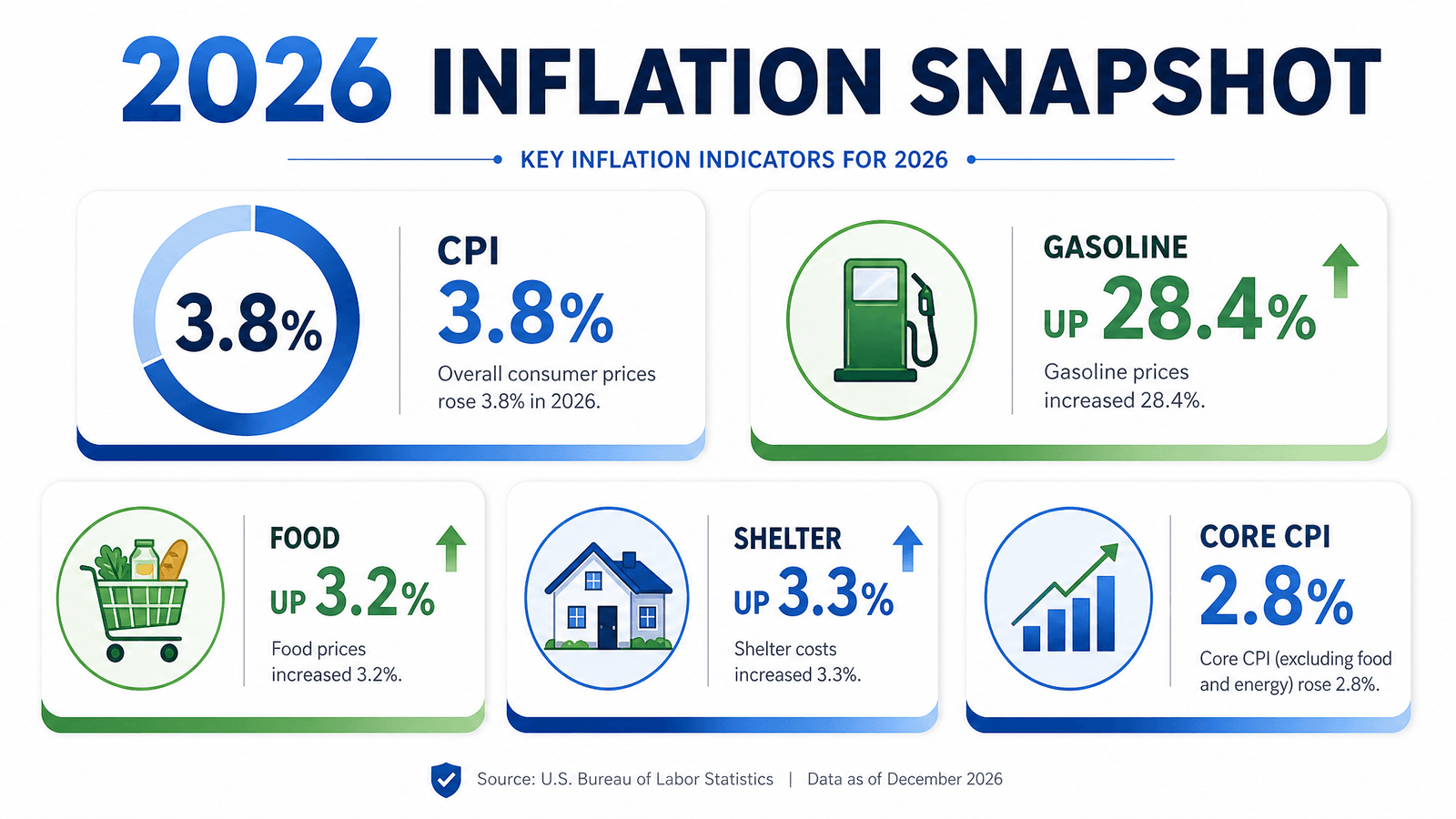

In April 2026, the Consumer Price Index (CPI) jumped to 3.8% year-over-year, the highest reading since May 2023. Energy prices surged 28.4% over the past year, food costs climbed 3.2%, and shelter costs — already painfully high — rose another 3.3%. If you’ve been wondering why your paycheck doesn’t seem to stretch as far as it used to, the numbers confirm what your gut already knew.

At Your Career Place, we believe that understanding the economic forces shaping your financial life is the first step toward taking control of it. So this week, we’re diving deep into inflation: where it stands, where it’s headed, and — most importantly — what you can do about it right now. As always, we’ll look at this through two lenses: the Boomer (optimistic) perspective and the Doomer (pessimistic) perspective, because the truth, as usual, lives somewhere in between.

The Inflation Landscape: What the Numbers Actually Say

Before we get into the debate, let’s ground ourselves in the data. Here’s a snapshot of where inflation stands as of mid-2026:

- Headline CPI: 3.8% year-over-year (April 2026) — the highest since May 2023

- Core CPI (excluding food and energy): 2.8% — more moderate, but still above the Fed’s 2% target

- PCE Price Index (the Fed’s preferred gauge): 3.8% headline, 3.3% core

- Gasoline prices: Up 28.4% over the past year

- Food at home: Up 3.2% annually, with forecasts of 4.0–4.5% for the full year

- Shelter costs: Up 3.3% annually, with 30-year mortgage rates hovering around 6.3%

What’s driving all of this? A few key culprits: geopolitical conflicts that have sent energy prices soaring, tariffs on imported goods that businesses are now passing on to consumers (after absorbing them in 2025), a persistent housing affordability crisis, and supply chain pressures that haven’t fully resolved. The Federal Reserve, meanwhile, has kept its benchmark interest rate steady in the 3.50%–3.75% range, and major financial institutions like Goldman Sachs and Nomura are now forecasting that rate cuts won’t arrive until 2027 — if at all.

The bottom line: inflation is real, it’s sticky, and it’s not going away overnight. But how you interpret that reality — and what you do about it — depends a lot on your financial situation and your mindset.

The Boomer Perspective: “This Is a Speed Bump, Not a Cliff”

If you’re in the optimistic camp, here’s the case for keeping your cool — and even finding opportunity in the current environment.

First, the economy is still growing. Real GDP expanded at a 2.0% annual rate in Q1 2026, and the unemployment rate sits at 4.3% — historically low by any measure. The labor market, while cooling slightly, has not collapsed. People are still working, businesses are still hiring, and consumer spending, though strained, continues.

Second, core inflation is more moderate than the headlines suggest. That 3.8% headline number is heavily influenced by energy — a notoriously volatile category. Strip out food and energy, and core CPI is running at 2.8%. That’s still above the Fed’s 2% target, but it’s a far cry from the 9% peak we saw in 2022. The trend, while bumpy, is generally downward.

Third, for investors, this environment has actually been rewarding. The S&P 500 delivered a strong 16.4% return in 2025, and the AI-driven technology sector continues to attract capital. For those with diversified portfolios, rising asset prices have helped offset some of the sting of higher consumer prices. High-yield savings accounts and CDs are still offering yields above 4% — a genuine opportunity to earn a real return on cash that simply didn’t exist a few years ago.

Fourth, the Federal Reserve has a plan. Yes, rate cuts have been pushed back. But the Fed’s steady hand — holding rates firm rather than panicking — signals institutional confidence that inflation will eventually be tamed. When cuts do come (likely in 2027), those who locked in higher yields on bonds and CDs will look very smart indeed.

The Boomer takeaway? Stay invested, stay disciplined, and don’t let fear drive your financial decisions. Inflation is a challenge, but it’s a manageable one for those who plan ahead. At Your Career Place, we’ve seen this movie before — and the ending, for patient investors, tends to be a good one.

The Doomer Perspective: “The Affordability Crisis Is Getting Worse”

Now let’s be honest about the harder reality that millions of Americans are living right now.

The most alarming data point in the current inflation picture isn’t the headline CPI — it’s what’s happening to real wages. As of April 2026, real average hourly earnings fell 0.3% year-over-year. That means the average worker’s paycheck is buying less than it did a year ago. When prices rise faster than wages, the math is brutal: you’re effectively taking a pay cut without anyone telling you.

And the savings cushion that many households built up during the pandemic? It’s gone. The personal savings rate dropped to just 2.6% in April 2026 — its lowest level since mid-2022. Total household debt has hit a staggering $18.8 trillion. Between 51% and 67% of Americans report living paycheck to paycheck. These aren’t abstract statistics — they represent real families making impossible choices between groceries, rent, and credit card minimums.

The inflation burden is also deeply unequal. Lower-income households spend roughly 43% of their budget on housing and another 16% on food. For the highest earners, those figures are 29% and 10%, respectively. When shelter and food prices spike, it functions as a regressive tax — hitting those who can least afford it the hardest. And with credit card APRs averaging around 25%, any household that has turned to plastic to bridge the gap is now paying a devastating price.

The housing market offers little relief. Yes, home price growth has moderated, but with mortgage rates near 6.3% and rents still elevated, the dream of homeownership feels further away than ever for many younger and middle-income workers. And the tariff pass-through that’s now hitting consumer goods — furniture, apparel, packaged foods — is adding insult to injury.

The Doomer takeaway? This is not a time for complacency. If you’re feeling squeezed, your instincts are correct. The structural forces driving up the cost of essentials — housing, food, energy, insurance — are not going away quickly. Defensive financial moves aren’t pessimism; they’re survival.

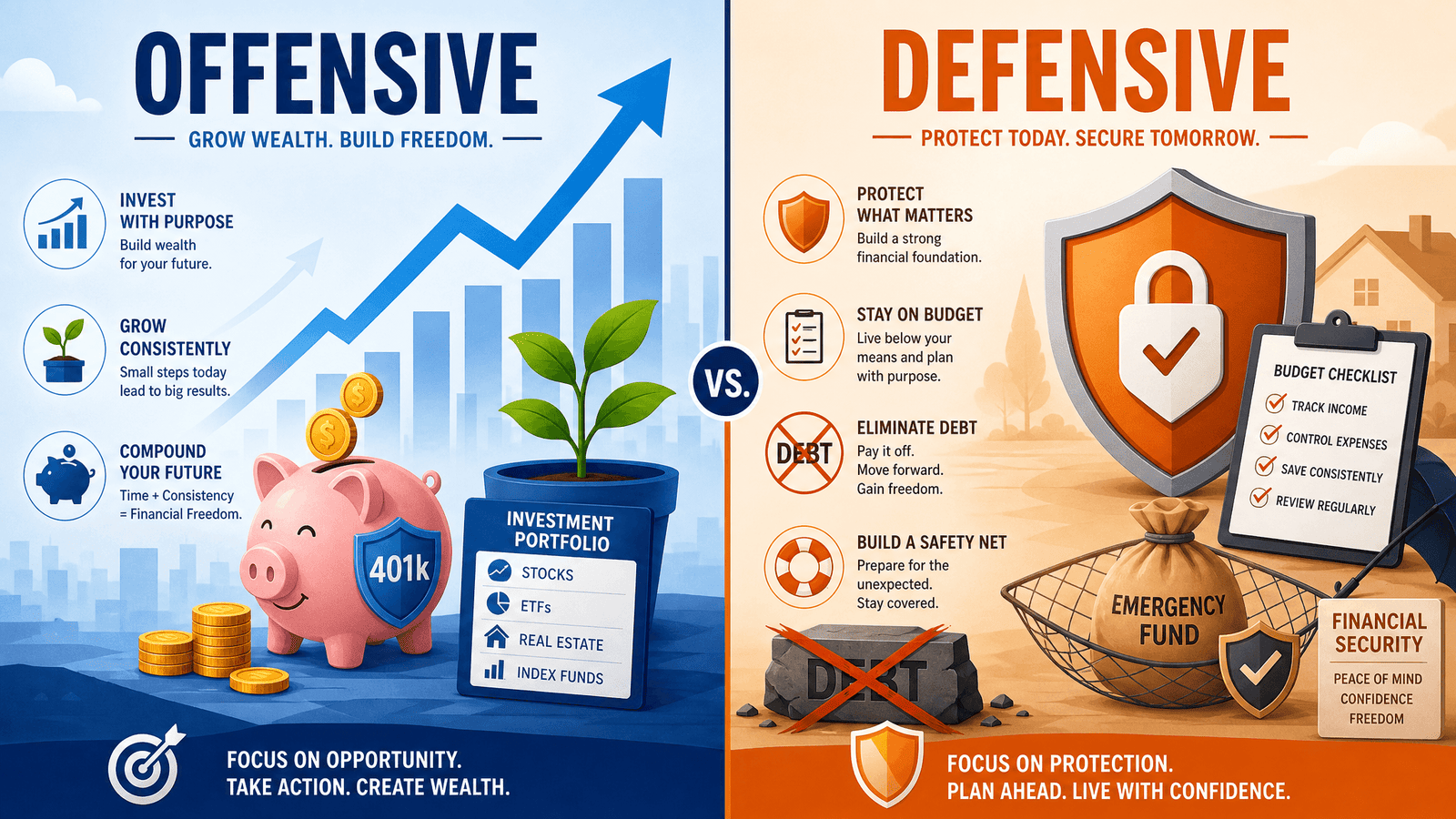

Key Takeaways: What You Can Do Right Now

Whether you lean Boomer or Doomer, the good news is that there are concrete steps you can take today to protect and grow your financial position. Here’s what the experts — and the data — suggest:

🚀 Offensive Moves (For the Optimists)

- Invest to outpace inflation. With core inflation near 3%, cash sitting in a low-yield account is losing value every day. Consider dividend growth ETFs (like DGRO) or broad index funds that have historically outpaced inflation over the long term. The AI-driven technology and infrastructure sectors continue to attract strong investment flows.

- Max out your retirement contributions. The 2026 limits are generous: $24,500 for 401(k)/403(b) plans and $7,500 for IRAs. Every dollar you contribute reduces your taxable income and compounds tax-advantaged over time. If your employer offers a match, that’s an instant 50–100% return on those dollars — don’t leave it on the table.

- Lock in high yields before rates fall. Online banks are still offering high-yield savings accounts and CDs above 4%. When the Fed eventually cuts rates (likely 2027), these yields will drop. Locking in now — especially with longer-term CDs — is a smart move for your emergency fund and short-term savings.

🛡️ Defensive Moves (For the Realists)

- Build a rigorous budget — and actually stick to it. Zero-based budgeting, where every dollar is assigned a purpose, is one of the most powerful tools available. Apps like YNAB, EveryDollar, or Monarch Money can help you track spending, identify subscription creep, and automate savings. The average American household spends over $10,000 a year on food, with nearly 40% of that on dining out — a powerful lever to pull.

- Attack high-interest debt with urgency. With credit card APRs averaging 25%, paying down that balance is the equivalent of earning a guaranteed 25% return. Use the avalanche method (highest APR first) or the snowball method (smallest balance first) — either works, as long as you’re consistent. If your credit allows, a 0% balance transfer card can buy you breathing room.

- Fortify your emergency fund. Aim for 3–6 months of essential living expenses in a liquid, high-yield savings account. The fact that many Americans struggle to cover a $400 emergency expense is a stark reminder of how quickly financial stability can unravel. This fund is your first line of defense.

- Review your insurance coverage. Insurance premiums — auto, home, health — have risen sharply. Shop around annually. Bundling policies, raising deductibles on lower-risk items, and comparing quotes can save hundreds of dollars a year.

The Bottom Line

Inflation in 2026 is a tale of two economies. For those with investments, stable incomes, and financial buffers, it’s a challenging but navigable environment with real opportunities. For those living paycheck to paycheck, it’s a genuine crisis that demands immediate, decisive action.

At Your Career Place, we believe that financial literacy is one of the most powerful career tools you have. Understanding inflation — not just as a news headline, but as a force that directly shapes your purchasing power, your savings, and your retirement timeline — puts you in the driver’s seat. Whether you’re playing offense or defense right now, the worst thing you can do is nothing.

Take one step this week. Open that high-yield savings account. Make an extra payment on your highest-interest debt. Increase your 401(k) contribution by even 1%. Small moves, made consistently, compound into life-changing results.

We’ll be back next week with more practical personal finance insights to help you build the career and financial life you deserve. Until then, keep learning, keep growing, and keep moving forward.

Sources: U.S. Bureau of Labor Statistics (BLS), U.S. Bureau of Economic Analysis (BEA), Federal Reserve, New York Fed, Goldman Sachs, Nomura, Redfin, National Association of REALTORS®, Ramsey Solutions, IRS, CBS News, CNBC, Reuters.

Tags: inflation, personal finance, budgeting, investing, Federal Reserve, cost of living, 2026 economy, Your Career Place