Retirement Planning in 2026

New Rules, Rising Costs, and What It All Means for You

By Your Career Place | May 13, 2026

Introduction: The Retirement Landscape Is Shifting — Are You Ready?

Retirement planning has never been a “set it and forget it” exercise, but 2026 is shaping up to be one of the most consequential years for retirement savers in recent memory. Between sweeping legislative changes from the SECURE 2.0 Act, fresh IRS contribution limits, a new Social Security cost-of-living adjustment, and sobering data about how much retirement actually costs, there’s a lot to unpack.

At Your Career Place, we believe that understanding your financial future is just as important as building your career. Whether you’re 25 and just starting to think about retirement, or 60 and counting down the years, the decisions you make right now can have a massive impact on the life you’ll live later. So let’s break down what’s new, what’s changing, and what it means for you — from two very different perspectives.

What’s New in 2026: The Headlines You Need to Know

The retirement planning world has been buzzing with significant updates. Here’s a quick rundown of the most important developments:

1. Higher Contribution Limits Across the Board

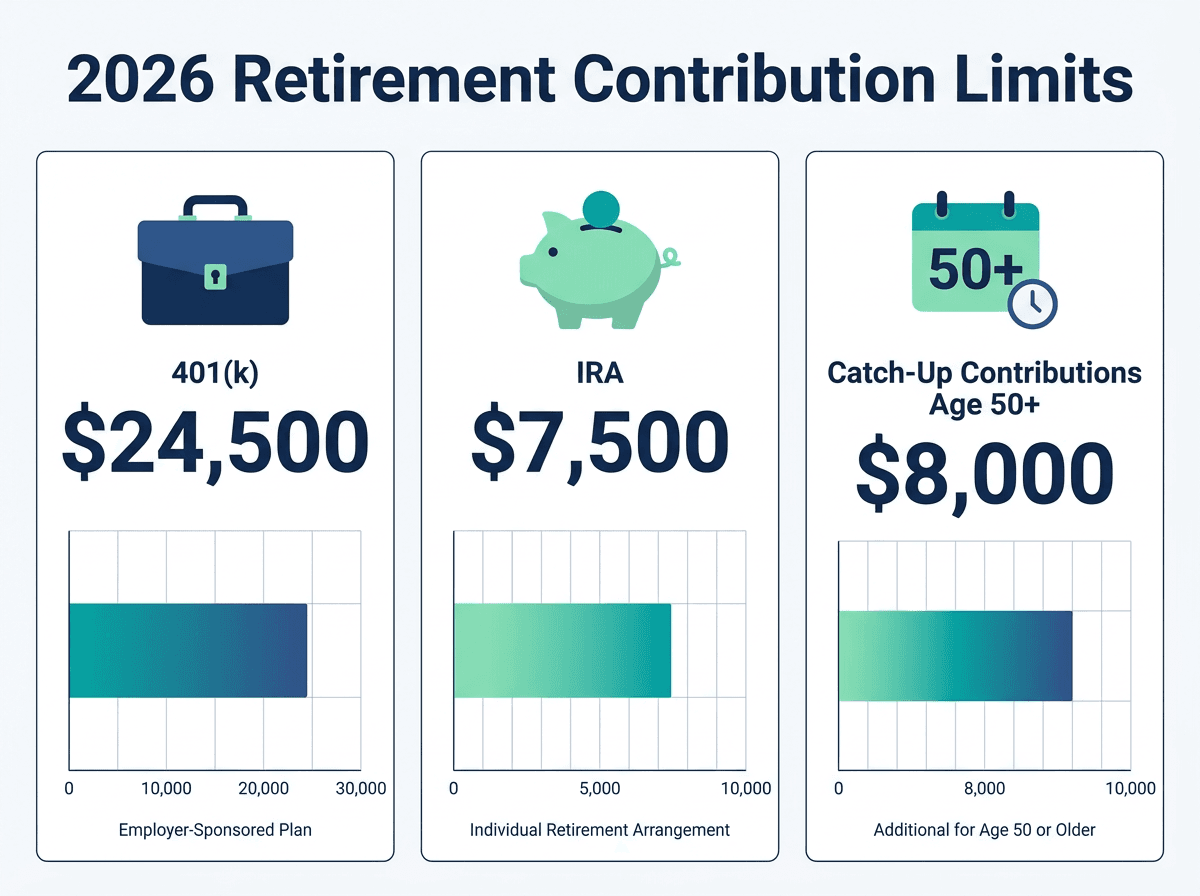

The IRS has raised the bar for how much you can save in tax-advantaged accounts. For 2026, the standard 401(k), 403(b), and Thrift Savings Plan contribution limit climbs to $24,500 (up from $23,500 in 2025). IRA savers get a bump too — the limit rises to $7,500, with a catch-up contribution of $1,100 for those 50 and older (now indexed to inflation for the first time). The total combined employee-plus-employer 401(k) limit hits a whopping $72,000.

2. The “Super Catch-Up” for Ages 60–63

Here’s a game-changer for late-career savers: if you’re between 60 and 63 years old, you can now make a “super catch-up” contribution of $11,250 to eligible workplace plans — significantly more than the standard $8,000 catch-up for those 50 and older. This provision, part of the SECURE 2.0 Act, is designed to help people in their early 60s turbocharge their savings in the final stretch before retirement.

3. Mandatory Roth Catch-Ups for High Earners

Starting January 1, 2026, if you earned more than $150,000 in the prior year, all your age-based catch-up contributions to a workplace plan must go into a Roth account (post-tax). This is a significant shift for high earners who previously preferred pre-tax contributions. The silver lining? Roth money grows tax-free and isn’t subject to required minimum distributions.

4. Social Security Gets a 2.8% Boost

The Social Security Administration announced a 2.8% cost-of-living adjustment (COLA) for 2026, adding roughly $56 per month to the average retired worker’s benefit. The taxable earnings maximum also rises to $184,500. While any increase is welcome, many retirees note that 2.8% barely keeps pace with the real-world costs they face — especially in healthcare and housing.

5. Automatic Enrollment Is Now the Law

New 401(k) and 403(b) plans established after December 29, 2022 must now automatically enroll eligible employees at a contribution rate between 3% and 10%, with automatic annual increases. This is a huge win for workers who might otherwise procrastinate on signing up — but it also means you should double-check your enrollment settings to make sure you’re contributing at the right level for your goals.

The Boomer Perspective: Reasons to Be Optimistic About Retirement in 2026

Let’s start with the good news — and there genuinely is some. If you’re a glass-half-full kind of person when it comes to retirement, here’s what’s working in your favor.

The rules are finally catching up to reality. For years, financial advisors have been saying that contribution limits weren’t keeping pace with inflation or the actual cost of retirement. The 2026 increases — especially the super catch-up for 60–63-year-olds — represent a meaningful acknowledgment that people need to save more, and the government is giving them the tools to do it. If you’re in that age bracket and can afford to max out, this is a golden opportunity.

Automatic enrollment is a behavioral game-changer. Research consistently shows that people who are automatically enrolled in retirement plans save significantly more over their lifetimes than those who have to opt in. The SECURE 2.0 mandate for automatic enrollment in new plans is expected to bring millions of workers — particularly younger and lower-income employees — into the retirement savings system who might otherwise have fallen through the cracks.

New flexibility tools are genuinely helpful. The student loan matching provision is a brilliant innovation: if you’re paying down student debt, your employer can now match those payments with retirement contributions. You don’t have to choose between your future and your present. Similarly, the ability to roll unused 529 funds into a Roth IRA (up to $35,000 lifetime) gives families more flexibility with education savings.

A personalized plan really does work. A recent Goldman Sachs survey found that retirees with a personalized retirement plan had a savings-to-income ratio 27% higher than those without one. And people with high “Financial Grit” — consistent habits like automating contributions and staying invested during market dips — accumulated 49% more in savings than peers with identical incomes. The message is clear: strategy and discipline pay off, literally.

At Your Career Place, we’ve always believed that career success and financial success go hand in hand. The same intentionality you bring to your professional development can transform your retirement outlook. The tools are there — it’s about using them wisely.

The Doomer Perspective: The Uncomfortable Truths About Retirement in 2026

Now for the reality check. Because as much as we’d love to paint a rosy picture, the data tells a more complicated story — and ignoring it won’t make it go away.

The retirement cost target keeps moving — and it’s moving fast. According to Northwestern Mutual’s 2026 Planning & Progress Study, the average American now believes they’ll need $1.46 million to retire comfortably — a 15% jump from the prior year’s estimate. Goldman Sachs projects that figure could balloon to $2.57 million by 2043, driven by longer life expectancies and rising annual costs. For context, the median retirement savings for Americans approaching retirement age is a fraction of that. The gap is not closing — it’s widening.

The “Financial Vortex” is real and it’s swallowing savings. Since 2000, housing costs as a percentage of income have surged from 21% to 36%. Family healthcare coverage has grown from 12% to 33% of income. These aren’t discretionary expenses — they’re the basics. And they’re crowding out retirement savings. A staggering 67% of workers report that monthly expenses prevent them from saving adequately for retirement. You can raise contribution limits all you want, but if people can’t afford to contribute, the limits are academic.

Healthcare costs in retirement are terrifying. A 65-year-old retiring in 2025 may need an average of $172,500 just for medical expenses throughout retirement — and that’s excluding long-term care. Long-term care costs can easily add hundreds of thousands more. Medicare covers some costs, but far from all. This is the retirement expense that most people dramatically underestimate, and it can derail even the best-laid financial plans.

Social Security’s 2.8% COLA isn’t keeping up. While any increase is better than none, a 2.8% COLA on an average benefit of roughly $2,000/month adds about $56. Meanwhile, the actual costs that retirees face — particularly healthcare, housing, and food — have been rising faster than the CPI-W measure used to calculate the COLA. Many retirees feel like they’re running on a treadmill: getting a raise every year but still falling behind.

The mandatory Roth catch-up could sting high earners. For workers earning over $150,000 who have relied on pre-tax catch-up contributions to reduce their current tax bill, the mandatory Roth requirement starting in 2026 means a higher tax bill today. Yes, the long-term benefits of Roth accounts are real — but the short-term cash flow impact is a genuine concern, especially for those in peak earning years with significant expenses.

Key Takeaways: What You Should Actually Do Right Now

Whether you lean Boomer or Doomer on the retirement outlook, the practical steps are largely the same. Here’s what Your Career Place recommends you focus on in 2026:

- Max out what you can — especially if you’re 60–63. The new super catch-up contribution limit is a limited-time opportunity. If you’re in that age window and have the financial capacity, take full advantage. Even a few extra years of maximized contributions can make a meaningful difference in your final balance.

- Check your automatic enrollment settings. If your employer has auto-enrolled you, don’t just accept the default contribution rate. Log into your plan and make sure you’re contributing enough to at least capture your full employer match — and ideally, as much as you can comfortably afford.

- Think about tax diversification. Having both pre-tax (Traditional) and post-tax (Roth) retirement accounts gives you flexibility in managing your tax burden in retirement. If you’re a high earner facing the mandatory Roth catch-up, consider it a nudge toward a more balanced tax strategy.

- Don’t forget about healthcare costs. Build a realistic estimate of your healthcare expenses in retirement into your planning. Consider a Health Savings Account (HSA) if you’re eligible — it’s one of the most tax-efficient vehicles available for covering future medical costs.

- Be strategic about Social Security. Delaying your Social Security claim from age 62 to 70 can dramatically increase your monthly benefit. For many people, this is one of the highest-return “investments” available. Run the numbers — or work with a financial advisor to do so.

- Create a written retirement plan. The Goldman Sachs data is compelling: people with a personalized plan save 27% more. It doesn’t have to be complicated. Write down your target retirement age, your income replacement goal (aim for 70–90% of pre-retirement income), and the specific accounts and strategies you’ll use to get there.

- Prepare for the non-financial side of retirement. Money is only part of the equation. Think about how you’ll spend your time, maintain social connections, and find purpose after your career ends. The happiest retirees are those who retire to something, not just from something.

Final Thoughts

Retirement planning in 2026 is a study in contrasts: more tools and opportunities than ever before, set against a backdrop of rising costs and persistent savings gaps. The SECURE 2.0 Act is genuinely moving the needle in the right direction, but legislation alone can’t close a gap that’s fundamentally driven by the rising cost of living.

The good news — and we mean this sincerely — is that you have more control than you think. The research is clear: people who make a plan, automate their savings, and stay disciplined through market ups and downs end up dramatically better off than those who don’t. It’s not about being lucky or earning a huge salary. It’s about being intentional.

At Your Career Place, we’re here to help you build not just a great career, but a great life — and that includes a financially secure retirement. Bookmark this page, share it with someone who needs it, and take one concrete step toward your retirement goals today. Future you will be grateful.

Sources: IRS.gov, Social Security Administration, Goldman Sachs Retirement Survey 2025, Northwestern Mutual 2026 Planning & Progress Study, J.P. Morgan Asset Management 2026 Guide to Retirement, Kiplinger, Fidelity, McLane Middleton, Human Interest, Vanguard.