Retirement Planning in 2026

Are You Ahead of the Curve or Behind the Eight Ball?

Let’s be honest — retirement planning is one of those topics that most of us know we should be thinking about, but somehow always ends up on the back burner. Between rising grocery bills, rent, and the general chaos of everyday life, saving for a future that feels decades away can seem like a luxury. But here’s the thing: 2026 is shaping up to be a genuinely pivotal year for retirement savers, and the decisions you make right now could have a massive impact on your financial future.

At Your Career Place, we believe that understanding your financial landscape is just as important as understanding your career landscape. So this week, we’re diving deep into the world of retirement planning — what’s changed, what’s at stake, and what you can actually do about it. Whether you’re 25 and just starting out or 55 and scrambling to catch up, there’s something here for you.

What’s New in Retirement Planning for 2026?

The retirement landscape has shifted significantly this year, with a mix of good news and sobering realities. Here’s a quick rundown of the most important developments:

1. Contribution Limits Just Got a Boost

The IRS raised the bar for how much you can stash away in tax-advantaged accounts. For 2026, you can now contribute up to $24,500 to your 401(k), 403(b), or 457 plan — up $1,000 from last year. IRA limits climbed to $7,500. If you’re 50 or older, the catch-up contribution for 401(k)s is now $8,000. And here’s the real headline: if you’re between ages 60 and 63, a brand-new SECURE 2.0 “super catch-up” provision lets you contribute a whopping $11,250 extra to your workplace plan. That’s a serious opportunity to turbocharge your savings in the final stretch before retirement.

2. Social Security Got a Raise — But Medicare Took a Bite

The Social Security Administration announced a 2.8% Cost-of-Living Adjustment (COLA) for 2026, bumping the average monthly benefit from $2,015 to about $2,071. Sounds great, right? Not so fast. Medicare Part B premiums jumped a steep 9.7%, from $185 to $202.90 per month. Since those premiums are deducted directly from Social Security checks, many retirees will see their net gain eaten up almost entirely by higher healthcare costs. The lesson? Don’t count on Social Security to keep pace with your actual expenses.

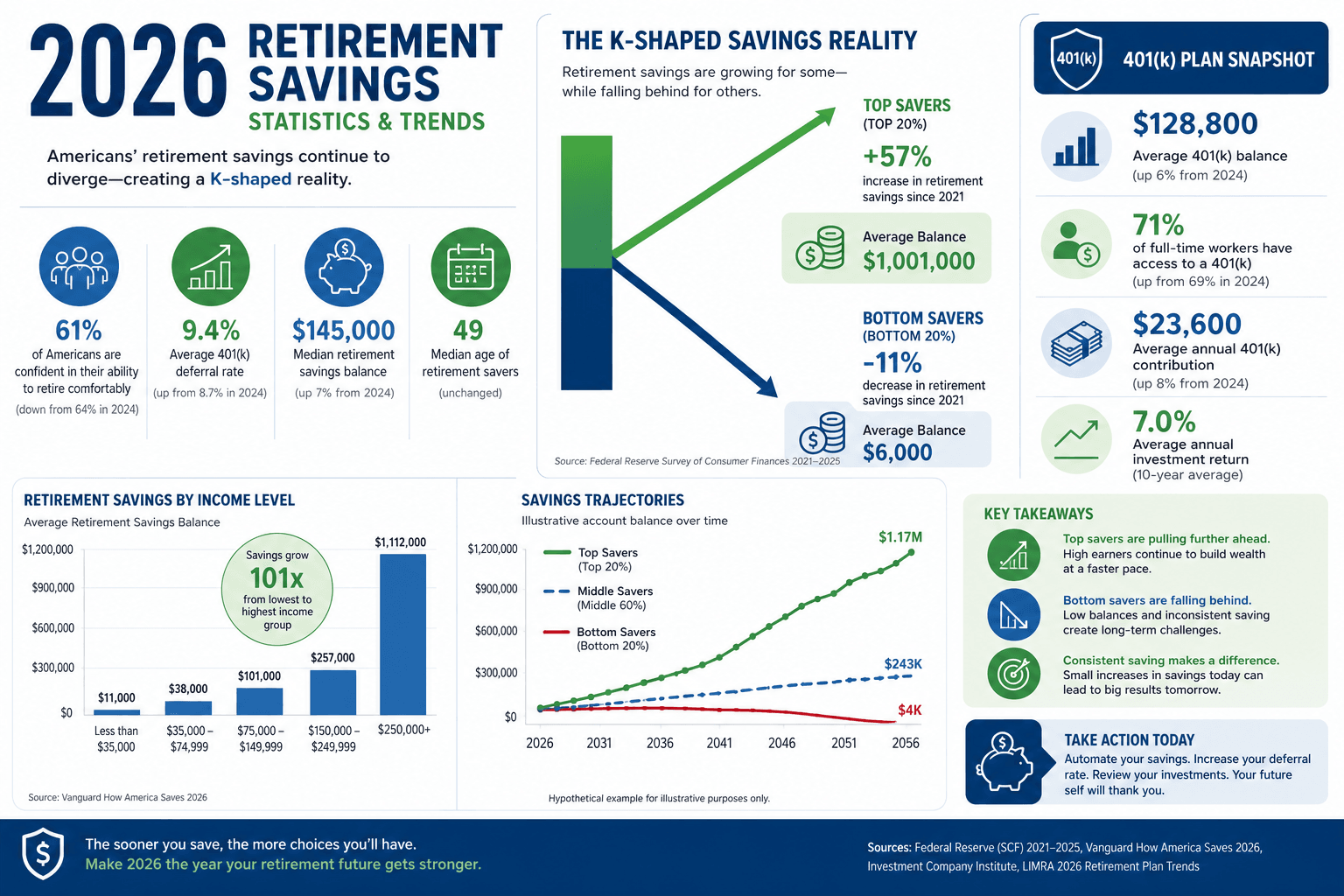

3. The “K-Shaped” Retirement Reality

Here’s where things get a little uncomfortable. Vanguard reported that the average 401(k) balance hit a record $167,970 at the end of 2025. Sounds impressive — until you look at the median balance, which is just $44,115. That median amount would generate roughly $147 per month under a standard 4% withdrawal rule. That’s not a retirement income; that’s a rounding error. Meanwhile, a record 6% of 401(k) participants took hardship withdrawals in 2025 — triple the pre-pandemic rate — raiding their future to survive the present.

4. SECURE 2.0 Keeps Rolling Out

The SECURE 2.0 Act of 2022 continues to reshape retirement accounts. Key 2026 provisions include mandatory Roth catch-up contributions for high earners (if you made over $150,000 last year and you’re 50+, your catch-up contributions must now go into a Roth account), expanded automatic enrollment in new workplace plans, and the introduction of Pension-Linked Emergency Savings Accounts (PLESAs) to help workers build a financial cushion without raiding their 401(k).

The Boomer Perspective: Reasons to Be Optimistic About Retirement in 2026

If you’re a glass-half-full kind of person — or a seasoned investor who’s seen markets rise and fall — there’s actually a lot to feel good about when it comes to retirement planning right now.

The tools have never been better. Higher contribution limits mean more room to grow your nest egg in tax-advantaged accounts. The new “super catch-up” provision for ages 60-63 is a genuine gift for late starters or anyone who wants to squeeze more into their retirement accounts before crossing the finish line. If you’re in that age bracket and haven’t looked into this yet, stop reading and call your HR department right now.

Markets have been rewarding patience. Despite all the economic noise, equity markets have continued to reward long-term investors. The record average 401(k) balance of nearly $168,000 didn’t happen by accident — it happened because people stayed invested through the volatility. Compound growth is still the most powerful force in personal finance, and time in the market continues to beat timing the market.

Innovation is on your side. The retirement industry is finally catching up to what retirees actually need: guaranteed income. Major firms like Vanguard, Fidelity, and BlackRock are now offering in-plan annuity options that let you convert a portion of your 401(k) into a personal pension — a steady paycheck for life. This is a game-changer for people who worry about outliving their savings.

Younger generations are getting smarter. Research shows that Gen Z and Millennials are starting to save for retirement nearly a decade earlier than their predecessors. Automatic enrollment, auto-escalation features, and better financial education are creating a generation of more prepared savers. That’s good news for the long-term health of the retirement system.

At Your Career Place, we’ve always believed that preparation beats panic. The optimistic case for retirement in 2026 is real: the legislative framework is improving, the tools are better than ever, and for those who are disciplined and proactive, the path to a comfortable retirement is absolutely achievable.

The Doomer Perspective: The Hard Truths You Need to Hear

Now let’s take off the rose-colored glasses for a moment, because the retirement picture in 2026 also has some genuinely alarming elements that deserve serious attention.

The median tells a different story. Yes, the average 401(k) balance is at a record high. But averages are deceiving. The median balance of $44,115 means that half of all 401(k) participants have less than that saved. For someone approaching retirement, that’s not a nest egg — it’s a nest twig. The gap between the retirement haves and have-nots is widening, and for millions of Americans, the math simply doesn’t add up.

Hardship withdrawals are a five-alarm fire. When 6% of 401(k) participants are raiding their retirement accounts just to stay afloat — and that number has been climbing for six straight years — something is deeply wrong. These aren’t people making bad financial decisions; these are people who have no other options. They’re paying taxes and penalties on money they desperately need now, while simultaneously destroying their future financial security. The emergency savings crisis is real, and it’s quietly gutting retirement accounts across the country.

Inflation is still the silent thief. While headline inflation has moderated, “sticky” inflation in housing, healthcare, and services continues to erode purchasing power. A 2.8% Social Security COLA sounds decent until you realize that Medicare premiums just went up 9.7%. For retirees on fixed incomes, the math is brutal. And for workers still saving, the cumulative price increases of the past few years mean that your retirement target number needs to be significantly higher than it would have been five years ago.

Most people don’t have a pension anymore. Only about 15% of private-sector workers have access to a traditional defined-benefit pension plan. Everyone else is on their own, navigating market volatility, sequence-of-returns risk, and the terrifying possibility of outliving their savings. The shift from pensions to 401(k)s transferred enormous financial risk from employers to employees — and most employees weren’t prepared for it.

Gen X is in trouble. Research from Northwestern Mutual shows that Generation X — those currently in their 40s and 50s — is more worried about affording retirement than any other generation. They’re caught in a financial squeeze: still paying off mortgages, funding college for their kids, and trying to accelerate retirement savings all at the same time. Many are behind where they need to be, and the window to catch up is closing.

Key Takeaways: What You Can Actually Do Right Now

Whether you lean Boomer or Doomer on the retirement outlook, the good news is that there are concrete steps you can take today to improve your situation. Here’s what the experts — and the data — suggest:

- Max out your contributions (or get closer to it). With 401(k) limits at $24,500 and IRA limits at $7,500, there’s more room than ever to grow your savings tax-advantaged. Even increasing your contribution rate by 1-2% can make a significant difference over time. If you’re 60-63, look into the new “super catch-up” provision immediately.

- Build an emergency fund — outside your 401(k). The record hardship withdrawal rate is a wake-up call. Your retirement account should be your last resort, not your first. Aim for 3-6 months of living expenses in a high-yield savings account. This one step could save you thousands in taxes and penalties — and protect your future self.

- Don’t assume Social Security will cover your needs. The 2.8% COLA sounds good until Medicare takes its cut. Plan for Social Security to be a supplement to your retirement income, not the foundation. Delay claiming if you can — every year you wait past 62 increases your benefit by roughly 6-8%.

- Inflation-proof your portfolio. Consider adding Treasury Inflation-Protected Securities (TIPS), dividend growth stocks, or REITs to your retirement portfolio. These assets can help your savings keep pace with rising prices over a 20-30 year retirement.

- Ask about in-plan annuity options. If your 401(k) plan now offers a lifetime income or annuity option, it’s worth understanding. Converting a portion of your savings into a guaranteed income stream can provide peace of mind and protect against the risk of outliving your money.

- Know your generation’s playbook. In your 20s-30s? Automate everything and let compound growth do the heavy lifting. In your 40s-50s? Maximize catch-up contributions and start planning for long-term care costs. In your 60s+? Focus on tax-efficient withdrawal strategies, Roth conversions, and optimizing your Social Security claiming strategy.

The Bottom Line

Retirement planning in 2026 is a tale of two realities. For those with the resources and discipline to take advantage of higher contribution limits, new legislative provisions, and innovative financial products, the path to a secure retirement has never been better-equipped. For those struggling with day-to-day financial pressures, the retirement gap is widening in ways that demand urgent attention — both personally and as a society.

At Your Career Place, we believe that knowledge is the first step toward action. Whether you’re just starting your career or counting down the years to retirement, understanding where you stand — and what tools are available to you — is the foundation of a solid financial future. The retirement landscape is complex, but it’s not impossible to navigate. Start where you are, use what you have, and take one step forward today.

Your future self will thank you.

This article is for informational purposes only and does not constitute financial advice. Please consult a qualified financial advisor for guidance tailored to your personal situation.