Real Estate in 2026

Is Now the Right Time to Buy, Sell, or Invest?

Key Takeaways

- In 2026, the housing market shows mixed signals: prices stabilize, inventory improves, but affordability remains a challenge.

- The Boomer perspective highlights potential growth with improved mortgage rates and regional hot spots offering opportunities.

- On the other hand, the Doomer perspective warns of high mortgage rates and an affordability crisis affecting many potential buyers.

- Investors should focus on cash flow rather than speculation, and consider REITs for diversification.

- Key takeaways emphasize local market research, pricing homes right, and maintaining financial health before buying or selling.

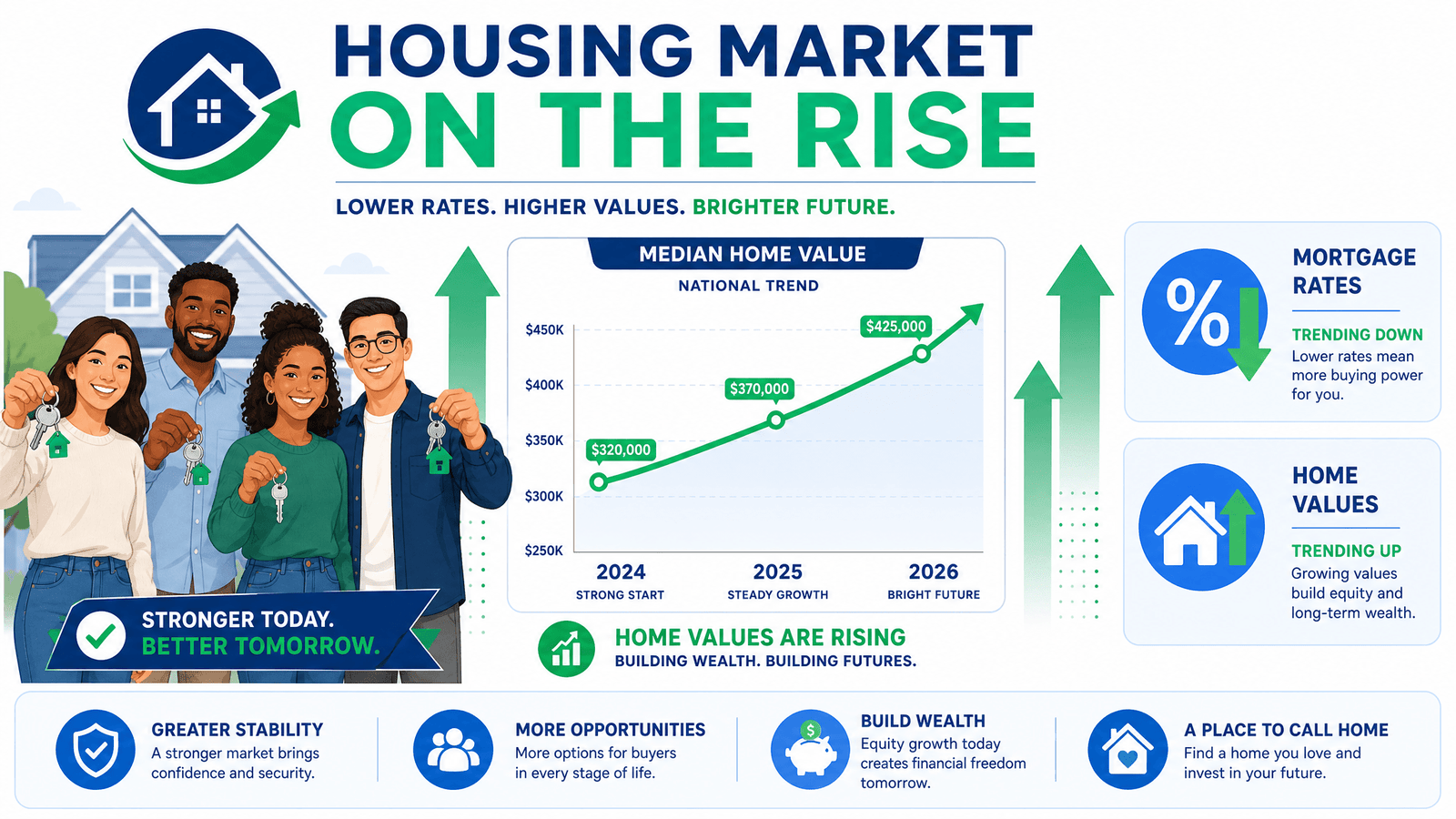

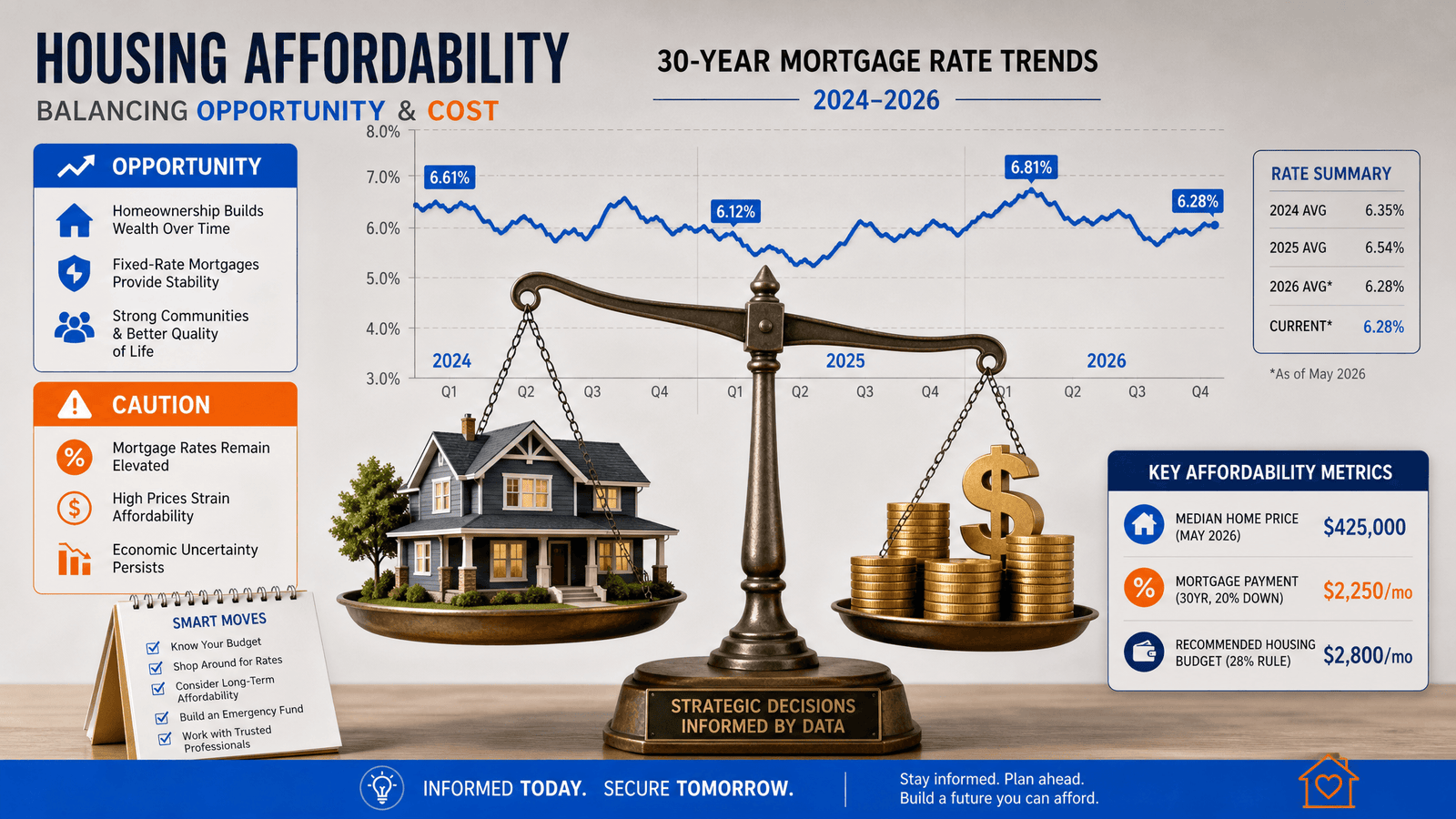

The American dream of homeownership has always come with a price tag — but in 2026, that price tag feels heavier than ever. Mortgage rates are still hovering above 6%, the median existing home costs over $429,000, and the headlines seem to flip between “housing market rebound!” and “affordability crisis deepens!” every other week. So what’s actually going on, and what does it mean for you?

Whether you’re a first-time buyer trying to get your foot in the door, a homeowner wondering if now is the time to sell, or a working professional looking to grow wealth through real estate investment, the mid-2026 housing market has something for everyone — including a healthy dose of confusion. At Your Career Place, we believe that cutting through the noise with real data and balanced perspectives is the best way to help you make smart financial decisions. So let’s do exactly that.

Where the Housing Market Stands Right Now

Before we dive into the debate, let’s ground ourselves in the numbers. Here’s a snapshot of the mid-2026 housing market:

- Median Existing-Home Price: $429,300 (NAR, May 2026)

- 30-Year Fixed Mortgage Rate: 6.43% (Freddie Mac, July 2, 2026)

- Existing-Home Sales: 4.17 million annualized rate (NAR, May 2026)

- Inventory: 4.5 months’ supply of existing homes; 10.3 months for new homes

- National Home Price Growth (Year-over-Year): +0.84% (S&P Case-Shiller, April 2026)

- Fannie Mae 2026 Price Forecast: +3.2% growth by year-end

The big picture? The market is in a period of recalibration. It’s not crashing, but it’s not booming either. Sales volumes are subdued, prices are growing modestly, and inventory is slowly improving — up roughly 20% year-over-year — giving buyers more options than they’ve had in years. But affordability remains a serious challenge, and the Federal Reserve has signaled that rate cuts are unlikely in 2026, meaning relief on the mortgage front isn’t coming anytime soon.

This is a market that rewards patience, preparation, and local knowledge. And it’s also a market where your perspective — optimistic or pessimistic — will shape the decisions you make. Let’s look at both sides.

The Boomer Perspective: “The Rebound Is Here — Don’t Miss It”

If you’re in the optimistic camp, 2026 looks like a genuine turning point for real estate. The National Association of REALTORS® (NAR) is forecasting a 14% jump in existing-home sales for the year, driven by easing mortgage rates and years of pent-up demand finally being released. That’s not a small number — that’s a meaningful shift in market activity.

Here’s the Boomer case in a nutshell:

Rates Are Easing (Slowly, But Surely)

Yes, 6.43% feels high compared to the 3% rates of 2021. But compared to the 7%+ rates of late 2023, we’re moving in the right direction. NAR economists estimate that a move toward 6% could qualify an additional 5.5 million households for homeownership. That’s 5.5 million potential buyers waiting on the sidelines — and as rates tick down, they’ll enter the market, supporting demand and prices.

Inventory Is Finally Improving

One of the biggest frustrations for buyers over the past few years has been the lack of homes for sale. That’s changing. Inventory is up 20% year-over-year, and new home inventory sits at a healthy 10.3 months’ supply. Homebuilders, eager to move product, are offering incentives like mortgage rate buydowns and closing cost assistance that simply weren’t available two years ago. For buyers willing to consider new construction, this is a genuine opportunity.

Home Prices Are Stable, Not Crashing

The Boomer perspective sees stable home prices as a feature, not a bug. A modest 1-4% annual appreciation protects existing homeowner equity without feeding speculative bubbles. If you buy today and prices grow 3% per year, you’re building wealth steadily — and if rates drop, you can refinance and lower your monthly payment. The fundamentals of homeownership as a long-term wealth-building tool remain intact.

Regional Hot Spots Offer Real Opportunity

NAR has identified ten “housing hot spots” for 2026 — markets like Minneapolis, Raleigh, and Columbus where inventory, job growth, and local incomes create more favorable conditions for buyers. Meanwhile, cities like Chicago are seeing 6.5% annual price gains, rewarding those who bought in the Midwest while others chased Sun Belt glamour. The lesson? Location still matters enormously, and smart buyers are finding value where others aren’t looking.

At Your Career Place, we often talk about the importance of playing the long game in your career — and the same principle applies to real estate. The Boomer perspective says: stop waiting for perfect conditions that may never come, and start building equity now.

The Doomer Perspective: “The Affordability Crisis Isn’t Going Away”

Now let’s be honest about the headwinds, because they’re real and they’re significant. The pessimistic view of the 2026 housing market isn’t doom-and-gloom for its own sake — it’s a sober assessment of structural challenges that aren’t going away anytime soon.

Mortgage Rates Are Still Punishing

A 6.43% mortgage rate on a $429,300 home (with 20% down) means a monthly principal and interest payment of roughly $2,150. Add property taxes, insurance, and maintenance, and you’re looking at $2,800–$3,200 per month in total housing costs. For many working professionals — especially those in high-cost-of-living cities — that’s simply not feasible. And with the Federal Reserve signaling no rate cuts in 2026, meaningful relief isn’t on the horizon.

The “Lock-In Effect” Is Strangling Supply

Here’s the cruel irony of the current market: millions of existing homeowners are sitting on 2.5–3.5% mortgage rates from 2020 and 2021. Selling their home means giving up that rate and taking on a new mortgage at 6.43%. For many, the math simply doesn’t work — so they stay put. This “lock-in effect” is keeping desirable existing homes off the market, limiting buyers’ choices, and keeping prices elevated even as demand softens.

Real Home Values Are Actually Declining

Here’s a data point the optimists don’t love: when you adjust home prices for inflation, real home values have been declining. The S&P CoreLogic Case-Shiller national index shows just +0.84% nominal growth year-over-year — which, when inflation is factored in, means homeowners are actually losing purchasing power. Several major markets are seeing outright price drops: Seattle is down 2.3% annually, with Phoenix, Denver, and Dallas also recording declines. If you bought in these markets at peak prices, you may be underwater or barely breaking even.

Affordability Is Near Historic Lows

The combination of high prices and elevated rates has pushed housing affordability to near-historic lows. The share of income required to purchase a median-priced home is well above the long-term average in most major markets. This isn’t just a problem for first-time buyers — it’s a structural issue that limits labor mobility, forces workers to commute longer distances, and concentrates wealth among those who already own property.

The Doomer perspective isn’t saying “never buy real estate.” It’s saying: go in with eyes wide open, understand the risks, and don’t let FOMO drive a decision that could strain your finances for decades.

A Tale of Two Markets: Regional Divergence in 2026

One of the most important things to understand about the 2026 housing market is that national averages can be deeply misleading. The market is bifurcated — performing very differently depending on where you look.

Markets showing strength: Chicago (+6.5% YoY), many Midwest and Northeast cities, and NAR-identified hot spots such as Minneapolis, Raleigh, and Columbus. These areas tend to have stronger job markets relative to home prices, better inventory, and less exposure to the pandemic-era speculative excess.

Markets cooling or correcting: Seattle (-2.3% YoY), Phoenix, Denver, Dallas, and other Sun Belt cities that saw explosive pandemic-era growth. These markets are now working through excess inventory and price corrections as the migration to remote work slows and local incomes struggle to support pandemic-peak prices.

The takeaway for working professionals: your local market is what matters. Before making any real estate decision, dig into the data for your specific city and neighborhood — not the national headline number.

Real Estate Investment in 2026: What’s Working

For those interested in real estate as an investment vehicle rather than a primary residence, the landscape is shifting in interesting ways.

REITs Are Rebounding: After underperforming in 2025, Real Estate Investment Trusts (REITs) are off to a strong start in 2026. For working professionals who want real estate exposure without the headaches of being a landlord, REITs offer a liquid, low-barrier-to-entry option. Sectors showing particular strength include data centers (fueled by demand for AI infrastructure) and senior housing (driven by an aging population).

Build-to-Rent Is the New Institutional Play: Large institutional investors are shifting away from buying existing single-family homes and toward developing entire communities of new homes expressly for rental. This “build-to-rent” (BTR) trend is expanding housing supply in some markets while also signaling that the smart money sees long-term rental demand as a safe bet.

The Rental Market Remains Resilient: The same affordability challenges that keep would-be buyers on the sidelines are also supporting rental demand. After a brief contraction, rent growth has turned positive again in many markets. For investors with existing rental properties, this is good news for cash flow.

At Your Career Place, we always emphasize that building wealth is a marathon, not a sprint. Real estate investment in 2026 rewards long-term thinking, cash-flow focus, and diversification — not speculation.

Key Takeaways: What Should You Actually Do?

Whether you’re buying, selling, or investing, here’s the practical guidance that matters most in the mid-2026 market:

If You’re Thinking About Buying:

- Focus locally, not nationally. Your neighborhood’s dynamics matter far more than the national average. Research inventory, price trends, and days on market in your specific area.

- “Marry the house, date the rate.” Waiting for 3% rates to return is not a strategy. Find a home that fits your life and budget now, and plan to refinance if rates drop significantly.

- Explore new construction. Builders are motivated to sell and offering real incentives — rate buydowns, price reductions, and closing cost assistance — that you won’t find in the resale market.

- Get financially fit first. A strong credit score and solid savings can unlock a lower interest rate, saving you tens of thousands over the life of your loan.

If You’re Thinking About Selling:

- Price it right from day one. The era of wildly over-asking offers is largely over. Overpricing is the surest way to have your home sit on the market and eventually sell for less.

- Condition is king. Buyers have more choices now. Move-in ready, well-maintained homes command a premium and sell faster. Invest in repairs and updates before listing.

- Understand your competition. More homeowners are being compelled to sell by life events (job changes, family growth, retirement), so you’ll face more competition than sellers did two years ago.

If You’re Thinking About Investing:

- Cash flow over speculation. Buying and flipping for quick profit is exceptionally risky in a flat-to-modest growth environment. Focus on long-term holds with positive cash flow.

- Consider REITs for diversification. Gain exposure to high-performing real estate sectors without the responsibilities of direct property management.

- Watch the condo market carefully. New FHFA rules requiring condo associations to maintain 15% of their annual budgets in reserves by 2027 could affect assessments and property values in condo-heavy markets.

The Bottom Line

The 2026 housing market is not in turmoil — it’s in transition. It’s finding a new, more sustainable equilibrium after years of pandemic-era volatility. For working professionals, that means the path to a successful real estate transaction is no longer paved with cheap money and guaranteed appreciation. Instead, it’s built on sound financial planning, deep local market knowledge, and a realistic understanding of both the opportunities and the challenges ahead.

Whether you lean Boomer or Doomer on the housing market, the most important thing you can do is make decisions based on your own financial situation, your local market conditions, and your long-term goals — not on fear, FOMO, or national headlines.

At Your Career Place, we’re here to help you navigate these decisions with clarity and confidence. Real estate is one of the most powerful wealth-building tools available to working professionals — but like any tool, it works best when you know how to use it. Stay informed, stay strategic, and as always, keep building toward the financial future you deserve.

Have questions about real estate, personal finance, or career growth? Explore more resources at Your Career Place and join the conversation.

Related links: