Can Your Household Budget Survive the Squeeze?

Budgeting in 2026

By Your Career Place | Personal Finance Series

Let’s be honest — talking about budgeting isn’t exactly the most thrilling topic at the dinner table. But in 2026, it might be the most important one. With inflation still running hot, credit card debt at record highs, and wages struggling to keep pace, the question isn’t just how you budget — it’s whether your current approach is even working anymore.

At Your Career Place, we believe that financial literacy is just as important as career skills. After all, what’s the point of earning more if you can’t hold onto it? This week, we’re diving deep into the state of household budgeting in 2026 — the good, the bad, and the downright alarming — and giving you both sides of the story so you can decide where you stand.

The Big Picture: What’s Happening to American Household Budgets Right Now

The numbers don’t lie, and right now they’re telling a complicated story. The Consumer Price Index rose 4.2% in the 12 months ending May 2026 — the largest annual jump since April 2023. Energy prices surged a jaw-dropping 23.5%, with gasoline alone up 40.5%. Food and shelter costs climbed 3.1% and 3.4%, respectively.

Meanwhile, real (inflation-adjusted) average hourly earnings actually fell by 0.7% over the same period. Translation: your paycheck is buying less than it did a year ago. The personal saving rate has dropped to just 3.0% — down from 4.5% at the start of the year — as households dip into savings or lean on credit just to cover the basics.

The debt picture is equally sobering. Total household debt hit a record $18.8 trillion in Q1 2026, and credit card delinquencies (90+ days past due) reached 13.12% — a 15-year high. An estimated 60–70% of Americans are living paycheck to paycheck, including roughly 40% of households earning over $100,000 a year.

And yet — here’s where it gets interesting — 53% of Americans now follow a formal budget, up from 46% in 2025. More people than ever are using AI-powered financial tools, cutting subscriptions, trading down to store brands, and embracing a new cultural movement called “loud budgeting.” So which story is the real one? Both, actually. Welcome to the tale of two economies.

🌞 The Boomer Perspective: “We’ve Been Through Tough Times Before — And We Always Come Out Ahead”

If you’re the type who sees a challenge as an opportunity, 2026 is actually a fascinating time to be a budgeter. Here’s why the optimists have a point.

More Americans Are Budgeting Than Ever

The fact that 53% of Americans now have a formal budget is genuinely encouraging. That’s a meaningful jump from 46% just a year ago, and it signals that people aren’t just throwing their hands up — they’re getting serious. Two-thirds of those budgeters say their primary motivation is making sure they can cover essentials. That’s not panic; that’s pragmatism.

Technology Is a Game-Changer

Here’s something that would have seemed like science fiction just a decade ago: over half of Americans now use AI-powered tools to manage their finances. We’re not talking about basic spreadsheets. Modern apps like Monarch Money, Copilot, and Origin function as full financial command centers — automatically categorizing transactions, detecting unused subscriptions, forecasting cash flow, and flagging spending patterns before they become problems.

At Your Career Place, we’ve long championed the idea that the right tools can transform your financial life. And right now, the tools available to everyday consumers are more powerful than anything a Wall Street analyst had access to 20 years ago. That’s a genuine reason for optimism.

People Are Getting Creative and Cutting Smart

Americans are adapting. Sixty-six percent of those expecting financial pressure are cutting back on dining out. Fifty-five percent plan to reduce subscription spending — and with the average American wasting $252 per year on unused subscriptions, that’s real money back in your pocket. Sixty-nine percent are buying store-brand products. These aren’t signs of defeat; they’re signs of financial intelligence.

The “loud budgeting” movement — where people openly declare their financial limits to friends and family rather than overspending to keep up appearances — is particularly refreshing. It’s a cultural shift that normalizes financial discipline, especially among younger generations who are tired of the social pressure to spend money they don’t have.

Long-Term Optimism Remains Strong

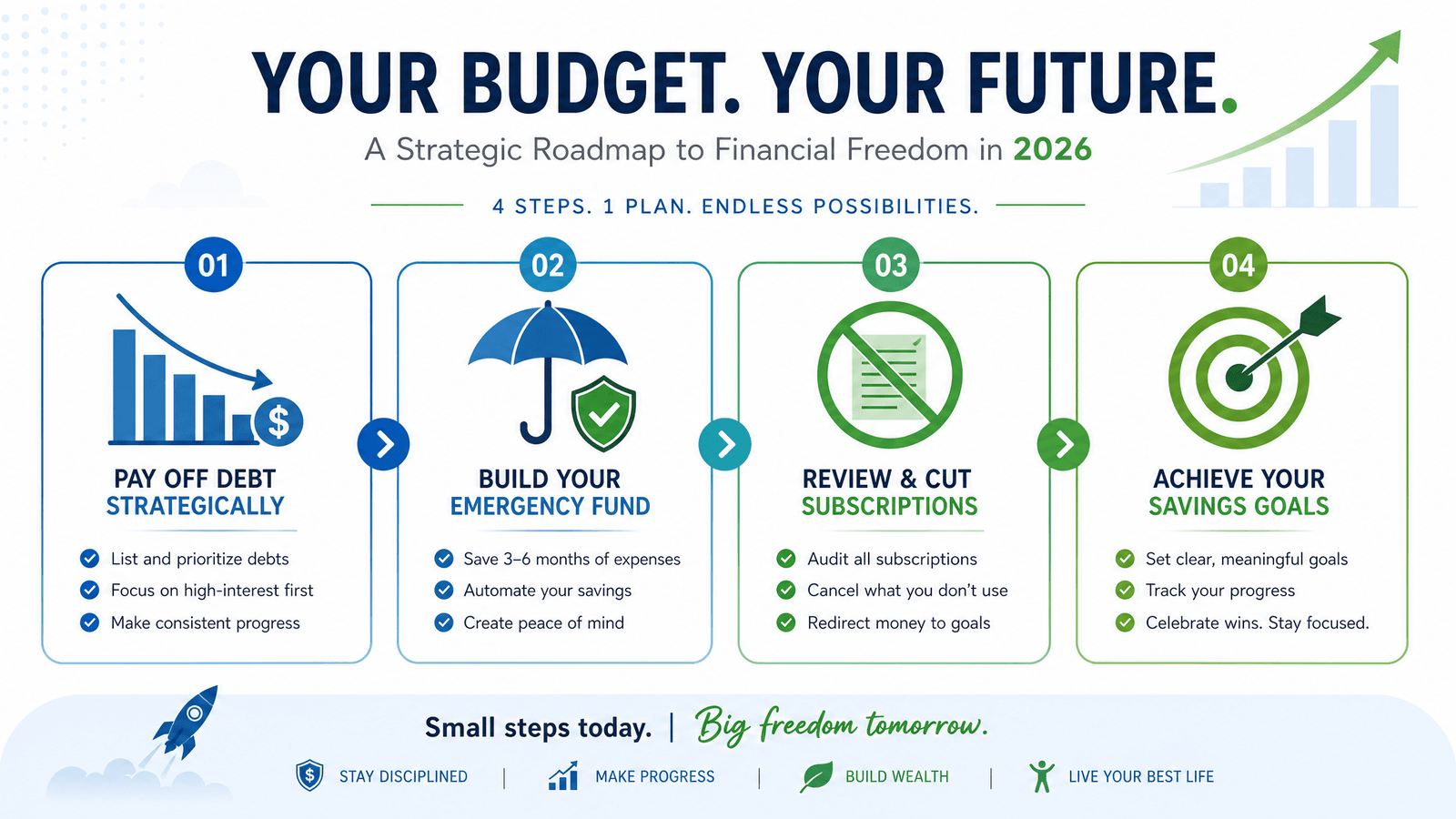

Despite the current squeeze, 74% of Americans believe they’ll be in a stronger financial position in five years. That’s not denial — that’s resilience. The classic budgeting strategies still work: the debt snowball, the debt avalanche, sinking funds for planned expenses, and automating your savings so you pay yourself first. These methods have helped Americans navigate recessions, oil crises, and financial panics for generations. They’ll work now too.

The bottom line from the Boomer camp: yes, it’s hard right now. But the tools, strategies, and mindset for building financial stability have never been more accessible. If you’re willing to put in the work, 2026 can be the year you finally get your budget under control.

🌧️ The Doomer Perspective: “The Math Just Doesn’t Add Up Anymore”

Now let’s hear from the other side — because ignoring the warning signs won’t make them go away.

Real Wages Are Losing the Race

Here’s the brutal truth: even if you got a raise this year, you probably got poorer. When inflation runs at 4.2% and your real wages drop 0.7%, no amount of budgeting creativity fully closes that gap. You can cut every subscription, switch to store brands, and stop eating out entirely — and you’re still fighting a losing battle against rising energy, food, and housing costs.

The personal saving rate at 3.0% is dangerously low. Financial experts generally recommend maintaining a savings rate of at least 10–15%. At 3%, most households have almost no buffer for unexpected expenses — and 76% of Americans have little to no emergency savings. Only 36% are confident they could cover an unexpected $2,000 expense. That’s a financial house of cards.

Debt Is Becoming a Way of Life

The rise of “survival debt” — using credit cards to pay for groceries and utilities — is one of the most alarming trends of 2026. When people are borrowing at 20–25% interest rates just to keep the lights on, they’re not building wealth; they’re digging a hole. And with credit card delinquencies at a 15-year high, many are already falling in.

The New York Fed has flagged a troubling “K-shaped” pattern: while higher-income households are managing, lower-income and subprime borrowers are experiencing a disproportionate deterioration in credit performance. The gap between those who are thriving and those who are struggling is widening, not narrowing.

The Classic Budgeting Rules Are Broken

Remember the 50/30/20 rule? Fifty percent for needs, 30% for wants, 20% for savings? For millions of Americans, that framework is now a fantasy. Essential “needs” — housing, food, transportation, utilities — are consuming 60–70% of household income for many families. There’s simply nothing left for the “wants” category, let alone meaningful savings.

Even the budgeting apps, as impressive as they are, can only optimize what’s there. If your income genuinely doesn’t cover your basic expenses, no AI tool can conjure money out of thin air. And the rise of Buy Now, Pay Later (BNPL) services — which the Consumer Financial Protection Bureau has explicitly warned about — is making it dangerously easy to paper over budget gaps with debt that compounds quickly.

Financial Stress Is at Crisis Levels

A staggering 88% of American adults report feeling financial stress in 2026. Twenty-two percent say they have nothing left at the end of the month. This isn’t just a personal finance problem — it’s a public health issue. Chronic financial stress is linked to anxiety, depression, relationship strain, and reduced workplace productivity. The human cost of this economic squeeze is enormous and largely invisible in the headline numbers.

The Doomer conclusion: budgeting is necessary but not sufficient. Without meaningful wage growth, relief from housing costs, or structural changes to the cost of essentials, even the most disciplined budgeter is running on a treadmill that keeps speeding up.

🔑 Key Takeaways: What You Can Actually Do Right Now

Whether you lean Boomer or Doomer, here are the concrete steps that financial experts are recommending for 2026 — and that the team at Your Career Place believes can make a real difference:

- Audit your subscriptions immediately. The average American wastes $252 a year on unused subscriptions. Do a “subscription freeze” — cancel everything, then only re-subscribe to what you genuinely miss. This is one of the fastest ways to find hidden money in your budget.

- Try a zero-based budget for 90 days. Apps like YNAB (You Need A Budget) or EveryDollar force you to assign every dollar a job. It’s intense, but it’s also the most effective method for people who feel like money just “disappears.” Give it three months before you judge it.

- Treat BNPL like a loan — because it is one. Before clicking “pay in 4,” ask yourself: does this payment fit in my existing budget? If the answer is no, don’t do it. The CFPB warns that “loan stacking” multiple BNPL plans is a fast track to financial distress.

- Build a sinking fund for planned expenses. Instead of being blindsided by car repairs, holiday gifts, or annual insurance premiums, divide the expected cost by the number of months until you need it and save that amount each month. It’s simple, but it eliminates a huge source of budget-busting surprises.

- Prioritize high-interest debt aggressively. If you’re carrying credit card balances at 20%+, that interest is destroying your budget. Use the debt avalanche method (highest interest first) to save the most money, or the debt snowball (smallest balance first) for psychological momentum. Either works — the key is to start.

- Adapt your budget framework to reality. If the 50/30/20 rule doesn’t work for your income level, try 60/20/20 or even 70/15/15. The goal isn’t to follow a rule perfectly — it’s to ensure you’re saving something and not accumulating debt for essentials.

- Leverage AI tools — but stay in charge. Apps like Monarch Money, Copilot, and Empower can automate the tedious parts of budgeting and surface insights you’d never catch manually. But remember: only 18% of Americans trust AI to make financial decisions autonomously, and that instinct is right. Use AI as a tool, not a replacement for your own judgment.

The Bottom Line

Budgeting in 2026 is harder than it’s been in years — but it’s also more important. The economic pressures are real, the debt levels are alarming, and the gap between income and expenses is genuinely painful for millions of families. At the same time, the tools, strategies, and community support available to today’s budgeter are more powerful than ever.

At Your Career Place, we believe that financial empowerment starts with honest information and practical action. Whether you’re just starting to track your spending or you’re deep in debt and looking for a way out, the most important step is the next one. Pick one strategy from this list, implement it this week, and build from there.

The economy may not be in your control. Your budget is.

Want more personal finance insights tailored to working professionals? Explore the full Your Career Place personal finance series and subscribe to our weekly newsletter for actionable tips delivered straight to your inbox.

Sources: U.S. Bureau of Labor Statistics (CPI, May 2026), U.S. Bureau of Economic Analysis (Personal Saving Rate, May 2026), New York Federal Reserve (Household Debt Report, Q1 2026), YouGov Consumer Spending Survey 2026, NerdWallet Subscription Survey 2026, CNET Subscription Survey 2026, Consumer Financial Protection Bureau (BNPL Guidance), National Endowment for Financial Education (NEFE) 2026 Poll, CivicScience Financial Distress Report 2026, Ramsey Solutions State of Personal Finance 2026.