Cryptocurrency in 2026: Boom, Bust, or Breakthrough?

What Every Working Professional Needs to Know

By Your Career Place | Personal Finance Series

If you’ve been watching the headlines lately, you know that cryptocurrency in 2026 is anything but boring. Bitcoin soared above $126,000 in late 2025, then crashed nearly 40% in a matter of weeks. Wall Street giants like Goldman Sachs and Morgan Stanley are now filing Bitcoin ETFs. The federal government finally passed a stablecoin law. And yet, $2 trillion in crypto market value was wiped out in just a few weeks at the start of this year.

So what does all of this mean for you — a working professional trying to build wealth, plan for retirement, and make smart financial decisions? At Your Career Place, we believe that staying informed is the first step to staying ahead. That’s why we’re breaking down the crypto landscape in plain English, with both the optimistic and the cautionary perspectives, so you can make decisions that actually fit your life.

Let’s dive in.

What’s Been Happening in Crypto: The 2026 Recap

The year started with a bang — and then a thud. Bitcoin entered January 2026 near $89,800 after touching an all-time high above $126,000 in late 2025. By February 5th, it had plummeted to around $63,295. That’s a drop of roughly 50% from peak to trough in just a few months. Along the way, approximately $2.5 billion in Bitcoin positions were liquidated in a single 48-hour stretch, and the total crypto market cap shed about $2 trillion.

But here’s the thing: the story of 2026 isn’t just about price swings. It’s about a fundamental shift in how crypto fits into the mainstream financial system. Here are the key developments every investor should know:

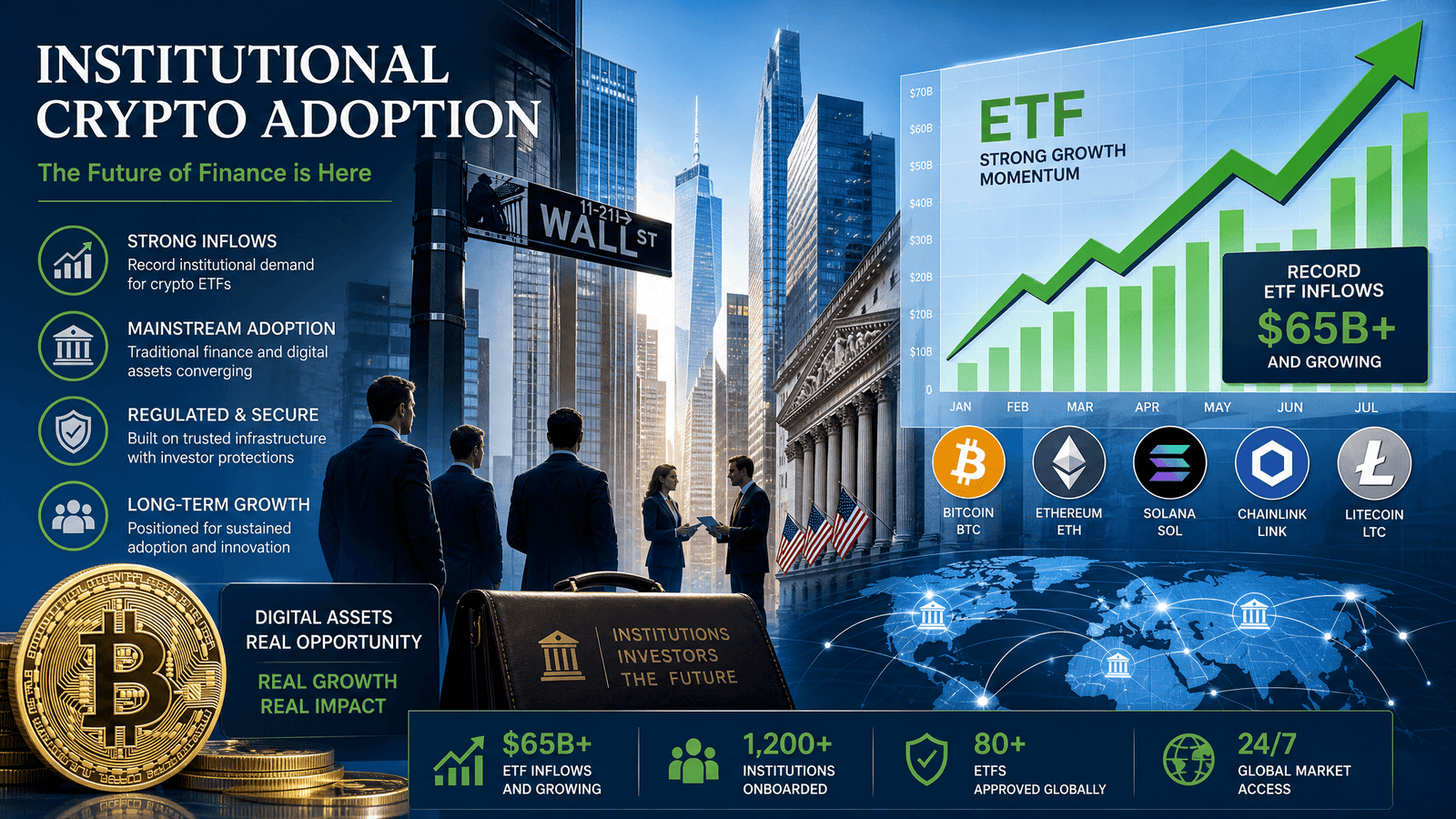

- The SEC got friendlier — fast. Under new Chair Paul Atkins, the SEC approved generic listing standards for crypto ETFs in September 2025, making it far easier for new crypto products to hit exchanges. In March 2026, the SEC and CFTC jointly released a “token taxonomy” that formally classified most crypto assets as not securities — a massive legal clarification that the industry had been waiting years for.

- Congress passed the GENIUS Act. This federal stablecoin law, enacted in July 2025, created a clear legal framework for USD-pegged digital tokens, requiring 1:1 reserves and carving compliant stablecoins out of securities laws. It’s the most significant crypto legislation in U.S. history.

- Wall Street went all-in. Morgan Stanley filed Bitcoin and Solana ETFs in January 2026. Goldman Sachs filed its first Bitcoin ETF product in April. BlackRock’s iShares Bitcoin ETF (IBIT) now holds roughly $67 billion in assets under management. Cumulative net inflows into U.S. spot Bitcoin ETFs have reached nearly $59 billion since their launch in early 2024.

- Crypto entered home finance. Coinbase and Better.com launched a program allowing homebuyers to use Bitcoin or USDC as down-payment collateral — a sign that crypto is creeping into everyday financial products.

By mid-2026, Bitcoin is down about 7% year-to-date, and analysts increasingly describe it as a “high-beta macro asset” — meaning it tends to move like a leveraged tech stock, rising sharply when risk appetite is high and falling hard when it isn’t.

The Boomer Perspective: Why Crypto Optimists Are Still Bullish

If you’re in the camp that sees crypto as a legitimate long-term investment — what we’re calling the “Boomer” perspective (not about age, but about the boom thesis) — there’s actually a lot to be excited about in 2026.

Regulatory Clarity Is Finally Here

For years, the biggest obstacle to mainstream crypto adoption wasn’t technology or demand — it was legal uncertainty. Businesses didn’t know if their tokens were securities. Exchanges didn’t know if they’d be sued. Investors didn’t know if their holdings were safe. That’s changing rapidly. Goldman Sachs identified regulatory clarity as the primary catalyst for the next wave of institutional crypto adoption, and the SEC’s new token taxonomy and the GENIUS Act are delivering exactly that.

Institutional Money Is Flowing In

When BlackRock, Goldman Sachs, and Morgan Stanley are all building crypto products, that’s not a fad — that’s infrastructure. The $58.7 billion in cumulative Bitcoin ETF inflows represents real institutional capital entering the space. For long-term investors, this kind of structural demand is a bullish signal. It means crypto is becoming a permanent fixture of diversified portfolios, not just a speculative side bet.

The Long-Term Thesis Remains Intact

Prominent analysts like Tom Lee of Fundstrat called for a new Bitcoin all-time high in early 2026, and while the timing hasn’t played out yet, the underlying thesis — that Bitcoin is a scarce, decentralized store of value in a world of expanding government debt — hasn’t changed. For investors with a 5-10 year horizon, the volatility of any given quarter matters far less than the long-term trajectory.

New On-Ramps for Everyday Investors

At Your Career Place, we know that accessibility matters. The good news is that getting exposure to crypto has never been easier or safer for the average investor. You can now buy Bitcoin ETFs through your regular brokerage account — no crypto wallet, no private keys, no exchange hacks to worry about. Charles Schwab, Bank of America, and JPMorgan all offer crypto ETF access alongside traditional portfolios. That’s a game-changer for working professionals who want a small allocation without the complexity.

The Doomer Perspective: Why Crypto Skeptics Have a Point

Now for the other side of the coin — the “Doomer” perspective. And honestly? The skeptics have some very valid arguments in 2026.

The Volatility Is Real and Brutal

A 40% drawdown from peak to trough in a matter of months is not a minor correction — it’s a financial earthquake. Bitcoin fell 6.5% in a single day on January 31st. The $2.5 billion in liquidations in early February wiped out leveraged investors overnight. If you had put a significant portion of your retirement savings into crypto at the 2025 peak, you’d be looking at devastating losses right now. This isn’t theoretical risk — it happened, and it will likely happen again.

It’s Not “Digital Gold” — It’s a Leveraged Tech Stock

One of the most compelling arguments for Bitcoin was that it would serve as a hedge against inflation and market turmoil — a “digital gold.” But 2026 has largely debunked that narrative. Bitcoin now trades as a high-beta macro asset, meaning it rises and falls with risk appetite, just like tech stocks. When the Fed gets hawkish, Bitcoin drops. When Treasury yields rise, Bitcoin drops. When investors rotate into AI stocks, Bitcoin drops. If you’re buying crypto as a hedge, you may be getting the opposite of what you bargained for.

Institutional Outflows Are a Warning Sign

Yes, institutional money has flowed into crypto ETFs — but it also flows out. In late May 2026, Bitcoin ETFs saw a record nine consecutive trading days of net outflows, totaling approximately $2.8 billion. A single institutional block trade of $1.29 billion was executed through a dark pool on May 26th. When the big players decide to rotate out of crypto and into AI or semiconductor stocks, retail investors are often left holding the bag.

The Retirement Math Doesn’t Add Up for Most People

Here’s a sobering statistic: Americans now believe they need $1.46 million to retire comfortably — up 15% from last year. Worker retirement confidence has fallen 6 points to 61%. In this environment, the temptation to chase high-return assets like crypto is understandable. But using volatile, speculative assets as a primary retirement vehicle is a dangerous gamble. The 2026 selloff is a reminder that crypto can take years to recover from a major drawdown — years you may not have if you’re close to retirement.

Crypto-Backed Products Come With Hidden Risks

The new Coinbase/Better.com crypto-backed mortgage program sounds innovative, but read the fine print: you need roughly $100,000 in Bitcoin to get $40,000 in down-payment credit. That’s a 2.5x collateralization ratio. If Bitcoin drops 40% — which it just did — you could face collateral calls at exactly the worst moment. These products are designed for sophisticated investors with substantial holdings, not for the average working professional trying to buy their first home.

Key Takeaways: What Should You Actually Do?

At Your Career Place, we’re not here to tell you whether to buy or sell Bitcoin. That’s your call, based on your own financial situation, risk tolerance, and goals. But we can offer some grounded, practical guidance based on what the experts are saying in 2026:

1. Build Your Foundation First

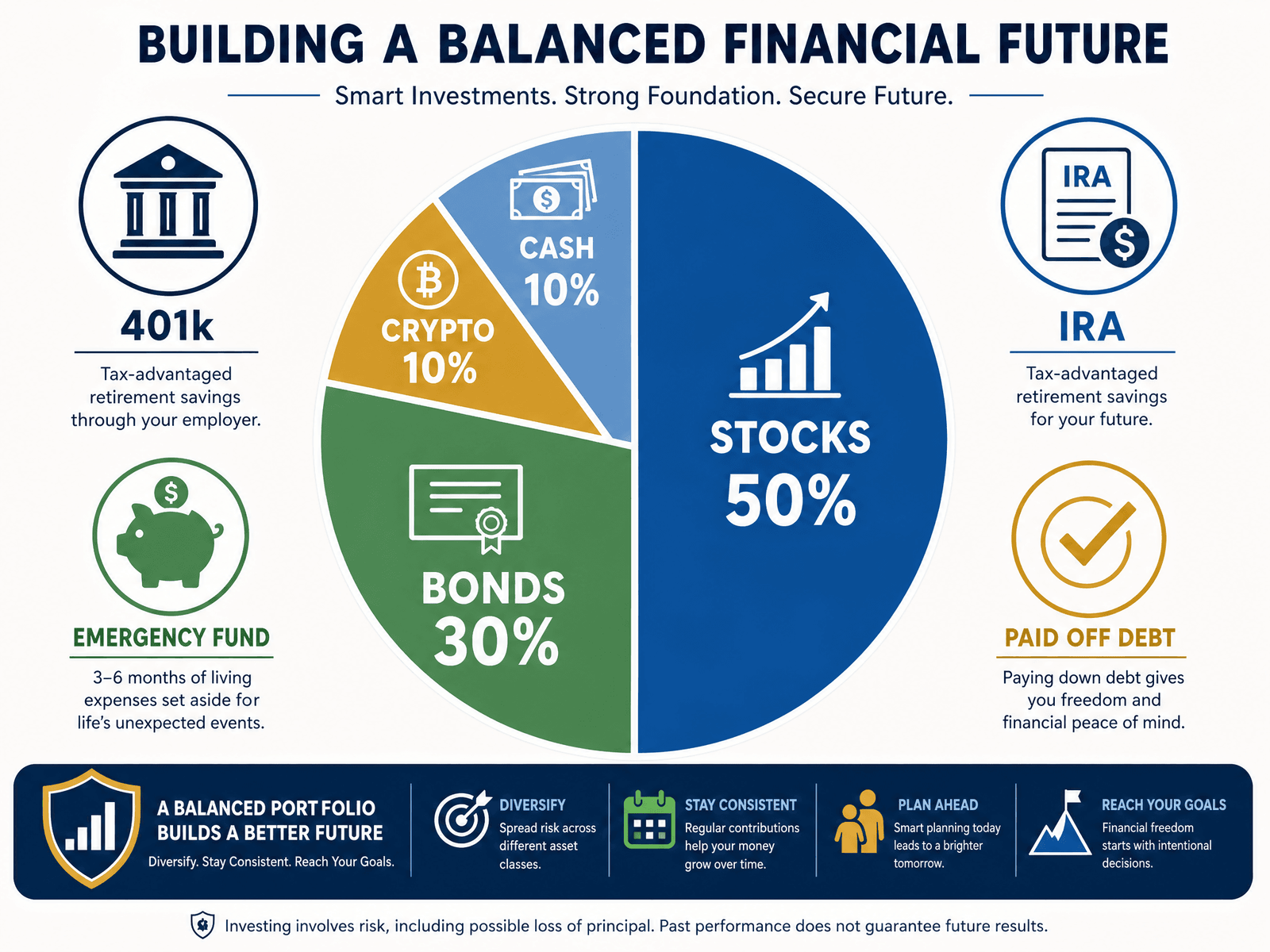

Before you put a single dollar into crypto, make sure you have: a 3-6 month emergency fund, your employer’s full 401(k) match captured, and your high-interest debt paid off. These are guaranteed returns. Crypto is not. The 2026 401(k) contribution limit is $24,500 (or $32,500+ with catch-up contributions for those 50+), and the IRA limit is $7,500. Max these out before you speculate.

2. Keep Crypto a Small Slice of Your Portfolio

Most financial advisors who are open to crypto recommend keeping it to no more than 5% of your total investable assets — and many say 1-3% is more appropriate. The 2026 selloff is a perfect illustration of why: a 40% drop in a 5% allocation hurts, but it doesn’t derail your retirement. A 40% drop in a 30% allocation is catastrophic.

3. Use Regulated Vehicles

If you want crypto exposure, the safest and simplest way is through a spot Bitcoin or Ethereum ETF in your regular brokerage account. You get the price exposure without the operational risks of self-custody, private keys, or exchange hacks. Avoid leveraged crypto ETFs — Morningstar predicts up to a fifth of the ~600 leveraged/inverse ETFs available may close in 2026 if volatility spikes.

4. Think Long-Term or Don’t Bother

Crypto is not a short-term trading vehicle for most people — it’s a long-term, high-risk, high-potential-reward allocation. If you’re going to invest, commit to a multi-year horizon and don’t check the price every day. The investors who got hurt most in early 2026 were those who bought near the top with money they couldn’t afford to lose.

5. Watch the Macro, Not the Memes

Bitcoin now moves with Fed policy, Treasury yields, and global risk appetite. If you want to understand where crypto is headed, pay attention to the same macro factors that drive stocks and bonds. Ignore the Twitter hype and the “to the moon” crowd.

6. Stay Skeptical of Crypto-Backed Financial Products

Crypto-backed mortgages, crypto savings accounts, and crypto lending products are proliferating in 2026. Approach them with extreme caution. The collateralization requirements are steep, the risks are complex, and the regulatory protections are still evolving.

The Bottom Line

Cryptocurrency in 2026 is more mainstream, more regulated, and more institutionalized than ever before. That’s genuinely good news for the long-term legitimacy of the asset class. But it’s also more volatile, more macro-sensitive, and more complex than many retail investors realize.

The sober middle path is clear: secure your financial foundation, max out your tax-advantaged retirement accounts, and if you choose to invest in crypto, do it with a small, regulated, long-horizon allocation that you can afford to lose. Don’t let the headlines — bullish or bearish — push you into decisions that don’t fit your actual financial situation.

At Your Career Place, we’re committed to helping you navigate the financial landscape with clear, honest, and practical information. Whether you’re just starting your career or planning your exit from it, the fundamentals of smart money management don’t change — even when the assets do.

Have questions about crypto or any other personal finance topic? Explore more resources at Your Career Place and take control of your financial future today.

Sources: Reuters, Bloomberg, SEC.gov, CoinDesk, Goldman Sachs Research, Coinbase 2026 Market Outlook, Northwestern Mutual 2026 Planning Progress Study, IRS.gov, Morningstar, Empower Financial, CBS News Money Moves 2026.